Financial Planning for Buying a Car in Singapore: A 2026 Roadmap

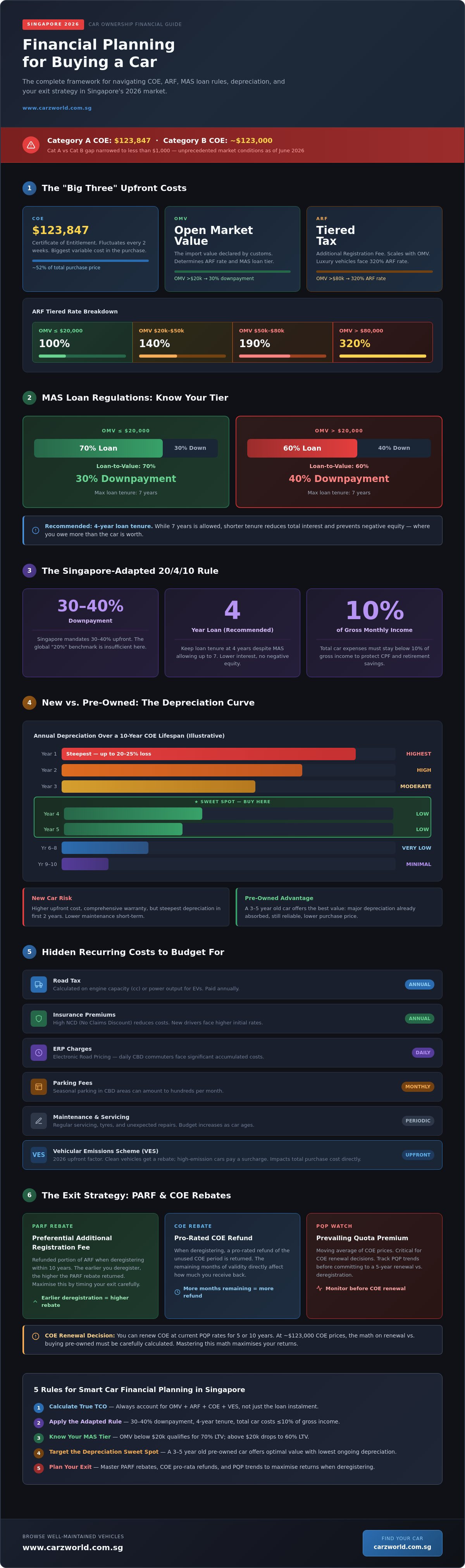

Would you still commit to a vehicle purchase if you knew that a Category A COE now costs $123,847? In 2026, the financial barrier to entry for car ownership in Singapore has reached unprecedented heights. Effective financial planning for buying a car is no longer just about saving for a downpayment. It's about navigating a complex maze of adjusted PARF rebates and tiered ARF rates that can catch even the most prepared buyers off guard.

It's natural to feel concerned about how these unpredictable costs impact your long-term stability. We're here to help you master the math with a clear framework designed for the current market. This roadmap provides a practical monthly budget breakdown and clarifies loan eligibility under the latest MAS regulations. We'll also explore how the narrowed gap between Category A and B prices affects your choices. Finally, you'll learn how to minimize depreciation losses, ensuring your investment remains as efficient as possible.

Key Takeaways

- Learn how to calculate the true Total Cost of Ownership by accounting for the "Big Three" expenses: COE, OMV, and ARF.

- Effective financial planning for buying a car requires adapting the traditional 20/4/10 rule to meet Singapore's unique 30-40% downpayment mandates.

- Understand current MAS car loan restrictions and how OMV thresholds determine whether you qualify for a 60% or 70% loan-to-value limit.

- Identify the "sweet spot" for value by analyzing the steep first-year depreciation curve and the benefits of selecting a 3-5 year old pre-owned car.

- Plan your exit strategy by mastering the math behind PARF and COE rebates to maximize your returns at the end of your car's lifespan.

Understanding the Total Cost of Ownership (TCO) in 2026

Understanding the Total Cost of Ownership (TCO) is the essential first step for effective financial planning for buying a car. In Singapore, TCO represents the total sum of the purchase price, registration taxes, and estimated running costs over a 10-year period. You shouldn't just look at the monthly loan instalment. A comprehensive view includes the "Big Three" costs: the Open Market Value (OMV), the Additional Registration Fee (ARF), and the Certificate of Entitlement (COE).

The ARF is particularly significant when calculating your budget. It's a tiered tax that scales with the car's OMV. For cars with an OMV above $80,000, the ARF rate is 320%. This makes luxury vehicles significantly more expensive than budget-friendly options. Additionally, the Vehicular Emissions Scheme (VES) plays a major role in 2026. Depending on the car's emission levels, you'll either receive a rebate or pay a surcharge. This directly impacts your upfront capital requirements and is a core part of financial planning for buying a car.

To visualize how these costs fit into a realistic budget, watch this helpful video:

The COE Variable: Budgeting for Volatility

COE prices fluctuate every two weeks during bidding cycles. As of June 2026, the gap between Category A and Category B has narrowed to less than $1,000, with prices hovering around $123,000. This volatility means your purchasing power can change overnight. Many buyers find that the "all-in" price at a dealer is more manageable. It provides a fixed cost and saves you from the stress of DIY bidding. If you're considering renewing an existing car, keep an eye on the Prevailing Quota Premium (PQP) trends, which represent the moving average of COE prices.

Hidden Recurring Costs: Beyond the Monthly Instalment

Don't forget the recurring expenses that keep your car on the road. Annual road tax is calculated based on engine capacity or power output for electric vehicles. You'll also need to factor in insurance premiums. A high No Claims Discount (NCD) can lower your costs, but new drivers should expect higher initial rates. Finally, estimate your daily Electronic Road Pricing (ERP) charges and seasonal parking fees, especially if you commute to the CBD. These small daily costs often determine whether a car truly fits your long-term financial goals.

The 20/4/10 Rule: Adapted for the Singapore Market

The 20/4/10 rule is a classic benchmark for vehicle budgeting, but it requires a major overhaul to fit the local context. When you're doing financial planning for buying a car, you'll quickly realize the global 20% downpayment suggestion is unrealistic here. Under current MAS car loan regulations, you generally need to provide 30% to 40% of the purchase price upfront. This depends on whether the vehicle's Open Market Value (OMV) is above or below $20,000. It's a steep hurdle. Saving this initial capital is often the most challenging part of the process for first-time buyers.

The "4" in the rule refers to a four-year loan tenure. While Singapore allows for a maximum of seven years, a shorter tenure keeps your total interest payments lower. It also ensures you don't end up with "negative equity," where you owe more than the car is worth. Finally, the "10" suggests that your total car-related expenses shouldn't exceed 10% of your gross monthly income. This cap is vital. It prevents your vehicle from cannibalizing your retirement savings or CPF contributions. High-net-worth individuals might stretch these ratios, but for most, staying within these bounds ensures long-term stability.

Calculating Your Maximum Purchase Price

Don't start your search with a specific model. Instead, reverse-engineer your budget from your monthly disposable income. Consider the "opportunity cost" of your downpayment. That $60,000 to $100,000 could otherwise earn returns in the STI ETF or stay in your CPF Ordinary Account. Choosing a brand new car might involve higher upfront costs, but it often comes with lower maintenance requirements and comprehensive warranties during the first few years. You can explore our range of well-maintained vehicles to see which models fit within your calculated budget.

Emergency Funds and Maintenance Buffers

Owning a car requires more than just paying the loan. You should implement a "six-month rule," keeping enough cash to cover half a year of car expenses in case of income changes. Budget for major service milestones that typically occur in the fifth and seventh years of a car's life. A sinking fund involves setting aside a fixed monthly sum specifically to cover predictable wear-and-tear items like tires, brake pads, and battery replacements. This proactive approach to financial planning for buying a car prevents sudden repairs from derailing your personal finances.

Financing Options: MAS Rules and Loan Strategies

Navigating the regulatory environment is a cornerstone of financial planning for buying a car. The Monetary Authority of Singapore (MAS) sets strict Loan-to-Value (LTV) limits that dictate exactly how much you can borrow. If the car's Open Market Value (OMV) is $20,000 or less, you can secure a loan for up to 70% of the purchase price. For vehicles with an OMV exceeding $20,000, the cap drops to 60%. This means you must be prepared to pay the remaining 30% to 40% in cash or through your trade-in value upfront.

Beyond LTV limits, your Total Debt Servicing Ratio (TDSR) plays a critical role in loan approval. Banks must ensure that your total monthly debt obligations, including your car loan, don't exceed 55% of your gross monthly income. This calculation includes your mortgage, credit cards, and any existing personal loans. Many buyers find it helpful to consult a DBS guide on car ownership costs to see how these debt ratios impact their realistic purchasing power before visiting a showroom.

You generally have two choices for financing: bank loans or in-house dealer financing. Bank loans typically offer lower interest rates, ranging from 2.48% to 3.08% as of June 2026. In-house financing often starts higher, sometimes at 4.28%, but it may offer more flexibility for individuals with unique credit profiles or those who prefer a one-stop transaction. Always ask for a transparent breakdown of all processing fees and administrative charges before signing any agreement.

Interest Rates and Loan Tenures

Don't focus solely on the flat interest rate quoted in marketing materials. The Effective Interest Rate (EIR) is the true cost of your loan, as it accounts for the reducing balance of your principal over time. While the maximum 7-year tenure lowers your monthly instalment, it significantly increases the total interest paid over the life of the loan. Check the fine print for early settlement penalties. Most lenders charge a fee if you pay off the loan before the term ends, which can eat into your savings if you plan to upgrade your vehicle early.

Balloon Scheme vs. Standard Loans

A Balloon Scheme can make high COE prices feel more manageable by deferring the car's PARF value until the end of the loan. This results in lower monthly payments, which helps with immediate cash flow. However, it carries significant risk at the end of the 10-year cycle. You won't receive the PARF rebate as cash because it has already been used to offset your loan. Standard loans are generally better for those who want to build equity in their vehicle. They ensure you receive your full rebates when the car is eventually scrapped or exported, providing a cleaner exit strategy for your financial planning for buying a car.

New vs. Pre-Owned: A Depreciation Deep Dive

A car loses a significant portion of its value the moment it leaves the showroom. In the Singapore market, this first-year depreciation is the steepest cost any owner will face. When you're focused on financial planning for buying a car, you must decide whether you want to absorb this initial hit or let a previous owner take it for you. Choosing a pre-owned car that is three to five years old is often the "sweet spot" for value. By this stage, the rapid decline in value has leveled off, but the vehicle usually remains reliable and modern.

While used cars offer lower entry prices, the savings can be erased by unexpected repair bills. Older vehicles naturally require more frequent parts replacements. It's essential to factor in a maintenance buffer for items like suspension components or cooling systems that may be nearing the end of their lifespan. We recommend browsing our inventory of certified pre-owned vehicles to find options that have undergone rigorous quality checks.

The Financial Logic of Used Cars

To understand the true cost, use straight-line depreciation. Subtract the estimated scrap value from your purchase price and divide it by the remaining years of the COE. This gives you your annual "paper loss." You should also account for interest rate differences. Used car loan rates typically range from 2.78% to 3.08%, which is slightly higher than new car rates. This higher interest is a vital factor in your financial planning for buying a car. Always insist on a pre-purchase inspection to ensure you aren't buying someone else's mechanical problems.

Parallel Imports and Brand New Savings

Parallel Importers (PI) often provide a more affordable route to a brand new car compared to Authorized Dealers (AD). They source models from different regions, allowing them to offer lower entry prices. However, you must carefully evaluate their warranty packages. While an AD provides factory-backed support, a PI relies on their own workshops or third-party providers. You should also consider that AD cars often hold a slightly higher resale value after five years because buyers perceive "agent-maintained" cars as more trustworthy. Weigh these initial savings against the potential difference in your eventual exit price.

The Exit Strategy: Resale, Export, and Rebates

Your roadmap isn't complete until you plan for the day you stop driving your current vehicle. Successful financial planning for buying a car requires a clear understanding of what you'll get back at the end of the journey. In Singapore, this recovery usually comes from the Preferential Additional Registration Fee (PARF) and Certificate of Entitlement (COE) rebates. You should be aware of the 2026 Budget updates, which capped PARF rebates at $30,000 and reduced the rebate rate to 5% for cars deregistered between nine and ten years of age. These changes mean you'll recover less upfront capital than owners did in previous years.

If your car is still in good mechanical condition, you don't have to settle for local scrap value. Choosing to export your car can often yield a higher body value, especially for popular models in international markets. This residual value serves as a vital financial bridge. By recouping these funds, you can significantly offset the high downpayment required for your next purchase, keeping your long-term mobility sustainable and within budget.

Maximizing Resale Value

Think of your maintenance records as a financial asset. A full service history can add thousands to your eventual selling price because it builds trust with the next buyer. Certain models, such as Toyota MPVs and Honda SUVs, traditionally hold their value better due to high local demand. Timing is also critical. You should aim to schedule your car sale during periods of rising COE prices. When new car prices climb, the demand for quality used vehicles typically follows, giving you better leverage in negotiations.

The 10-Year Decision: Scrap or Renew?

When your car hits the 10-year mark, you face a choice: scrap it or renew the COE. This decision depends on the Prevailing Quota Premium (PQP), which is the moving average of COE prices. Renewing the COE on a car that has already lost its PARF value can be a savvy budget move. Since you have no rebate left to lose, your only financial risk is the cost of the PQP and ongoing maintenance. The paper value of a car at the end of its first 10-year cycle is the guaranteed sum of the PARF rebate and any remaining pro-rated COE value. Understanding this figure is the final piece of financial planning for buying a car, ensuring you exit your investment with as much capital as possible.

Take the Next Step Toward Confident Ownership

Owning a vehicle in Singapore is a significant commitment that requires precise financial planning for buying a car. You now have the tools to calculate the true Total Cost of Ownership by accounting for COE volatility and tiered ARF rates. By adapting the 20/4/10 rule to meet local MAS loan restrictions, you can protect your monthly cash flow and long-term savings. A well-timed exit strategy involving export or scrap rebates is just as vital as the initial purchase price.

At Carz World, we simplify these complex logistical processes for you. We have earned over 100+ positive client testimonials by providing expert handling of COE bidding and vehicle financing. Our team also offers direct export capabilities to ensure you maximize your car's resale value when it's time for an upgrade. We focus on making your transition feel seamless and positive.

Browse our curated range of value-packed pre-owned cars at Carz World to find a vehicle that aligns with your financial goals. Your journey toward reliable car ownership starts with a partner you can trust.

Frequently Asked Questions

What is the minimum downpayment for a car in Singapore in 2026?

The minimum downpayment is either 30% or 40% of the purchase price, depending on the vehicle's Open Market Value (OMV). For cars with an OMV of $20,000 or less, you must provide a 30% downpayment in cash or trade-in value. If the OMV exceeds $20,000, the requirement increases to 40%. This significant upfront cost is a primary focus for most people when starting their financial planning for buying a car.

How does COE affect my car loan eligibility under MAS rules?

The Certificate of Entitlement (COE) is included in the total purchase price used to calculate your Loan-to-Value (LTV) limit. While the COE doesn't change the LTV percentage, higher COE prices increase the total loan amount you require. This larger loan must still fit within your Total Debt Servicing Ratio (TDSR), which is capped at 55% of your gross monthly income. High COE prices can therefore limit the specific car models you're eligible to finance.

Is it financially better to buy a new parallel import or a used car?

A used car that's three to five years old typically offers better financial value due to lower annual depreciation. While parallel imports (PI) provide a lower entry price for a brand new vehicle, they don't avoid the steep first-year value drop. If your goal is to minimize paper loss, a well-maintained pre-owned vehicle is often the more efficient choice. You should always weigh these savings against the higher interest rates usually charged for used car loans.

What is the PARF rebate and how do I calculate it?

The Preferential Additional Registration Fee (PARF) rebate is a sum returned to you when you deregister a car before its ten-year mark. Under 2026 regulations, this rebate is capped at $30,000. For a car deregistered between its ninth and tenth year, the rebate is 5% of the ARF paid. Calculating this accurately is a vital part of financial planning for buying a car, as it determines your vehicle's final "paper value" at the end of its lifespan.

Can I use my CPF to pay for a car loan or downpayment?

You cannot use your Central Provident Fund (CPF) savings to pay for a car's downpayment or monthly loan instalments. Car ownership is considered a private expense rather than a social security need like housing or healthcare. All payments must be made using cash or through a bank loan. It's important to ensure your cash reserves are sufficient to cover the required downpayment without depleting your emergency funds or long-term retirement planning.

How much should I set aside for annual car maintenance in Singapore?

Owners should generally set aside between $1,000 and $2,000 annually for routine maintenance and minor repairs. This budget should cover two servicing sessions, tire rotations, and general wear-and-tear items. Older vehicles or those approaching major milestones, such as the seven-year mark, may require larger buffers for significant part replacements. Establishing a dedicated sinking fund helps you manage these costs without causing sudden stress to your monthly household budget.

What is the difference between OMV and ARF in my car’s price breakdown?

The Open Market Value (OMV) is the actual price paid for the car including purchase price, freight, and insurance. The Additional Registration Fee (ARF) is a tax calculated as a percentage of that OMV. As the OMV increases, the ARF rate rises through tiered brackets, reaching up to 320% for luxury models. This relationship is essential because the ARF significantly inflates the final purchase price and determines your eventual PARF rebate eligibility.

Does a hybrid or electric car offer better long-term financial value?

Hybrid and electric vehicles often offer superior long-term value due to significant rebates under the Vehicular Emissions Scheme (VES). These upfront savings can offset the higher purchase price of green technology. Electric vehicles also benefit from lower daily running costs and potentially reduced maintenance since they have fewer moving parts. However, you should check the specific road tax for high-power EVs, as it's calculated differently than for internal combustion engines.

Disclaimer

This content is provided for general informational purposes only. Readers are encouraged to independently verify important information.

In Same Category

- Financial Planning for Buying a Car in Singapore: A 2026 Roadmap

- Government Regulations for Car Ownership in SG: The 2026 Essential Guide

- Lemon Law for Used Cars in Singapore Explained: Your Rights as a Buyer

- Top-of-the-Chart Hybrid Cars in Singapore: The 2026 Buyer’s Guide

- The Impact of COE on Used Car Prices in Singapore: A 2026 Guide

Related by Tags

- Financial Planning for Buying a Car in Singapore: A 2026 Roadmap

- Government Regulations for Car Ownership in SG: The 2026 Essential Guide

- Top-of-the-Chart Hybrid Cars in Singapore: The 2026 Buyer’s Guide

- The Impact of COE on Used Car Prices in Singapore: A 2026 Guide

- Used Car Market Outlook Singapore 2026: Trends, COE Impact, and Value Shifts

- COE for Commercial Vehicles: The Complete 2026 Guide for Singapore Businesses

- Electric Cars (EV) in Singapore: The Ultimate 2026 Buying Guide

- Performance Cars for Sale in Singapore: The Enthusiast’s 2026 Buying Guide

- Luxury Sedan Used Cars in Singapore: The Complete 2026 Buyer’s Guide

- Best Compact SUV for City Driving in Singapore: The 2026 Urban Guide

- Used Japanese Cars for Sale: The Ultimate Singapore Buyer’s Guide for 2026

- Best 7 Seater SUV Singapore: The 2026 Family Guide to Space and Value

- The Ultimate Guide to Buying Continental Cars in Singapore (2026 Edition)

- Understanding the Vehicle Emission Scheme (VES) in Singapore: A 2026 Guide

- Bidding for COE Number in 2026: The Complete Strategic Guide for Singapore Car Buyers

- Cat A vs Cat B COE Difference: The Complete 2026 Singapore Guide

- COE Price Trend Analysis 2026: Is Now the Best Time to Buy a Car in Singapore?

- Japanese and Korean Cars in Singapore: The Ultimate 2026 Buying Guide

- What Affects Car Resale Value in Singapore? A 2026 Guide to Maximising Your Return

- Car Valuation Certificate in Singapore: Your Complete Guide to Official Vehicle Worth

- Selling a Car with an Outstanding Loan in Singapore: The 2026 Complete Guide

- Detailing Your Car for Higher Resale Value: The Ultimate Singapore Guide for 2026

- How to Prepare Your Car for Sale in Singapore: The Ultimate 2026 Checklist

- When to Sell Your Car in Singapore: The Strategic 2026 Guide to Maximizing Returns

- Car Dealership Financing vs Bank Loan in Singapore: The 2026 Comparison Guide

- Common Problems with Used Cars: The Singapore Buyer’s Guide to Avoiding Lemons

- The Master Used Car Inspection Checklist for Singapore (2026 Edition)

- Deregistering a Car for Export in Singapore: The 2026 Complete Guide

- Shipping a Car from Singapore: The Ultimate 2026 Export Guide

- NCD for Car Insurance Explained: How to Maximise Your Savings in Singapore (2026)

- Car Loan Early Settlement Penalty in Singapore: The Complete 2026 Guide

- Used Car Loan Interest Rates in Singapore (2026): A Complete Financing Guide

- How to Get Pre-Approved for a Car Loan in Singapore: The 2026 Complete Guide

- Used Car Loan Downpayment in Singapore: The 2026 Ultimate Guide

- Buying a Second Hand Porsche Macan in Singapore: The 2026 Ultimate Guide

- Used Lexus ES250 in Singapore: The Ultimate Buyer’s Guide for 2026

- Buying a Pre-Owned Audi A3 in SG: The Ultimate Owner's Guide for 2026

- Used Volkswagen Golf Singapore: The Ultimate 2026 Buying Guide

- Used Honda Stream for Sale in Singapore: The 2026 Buyer’s Guide