How to Get Pre-Approved for a Car Loan in Singapore: The 2026 Complete Guide

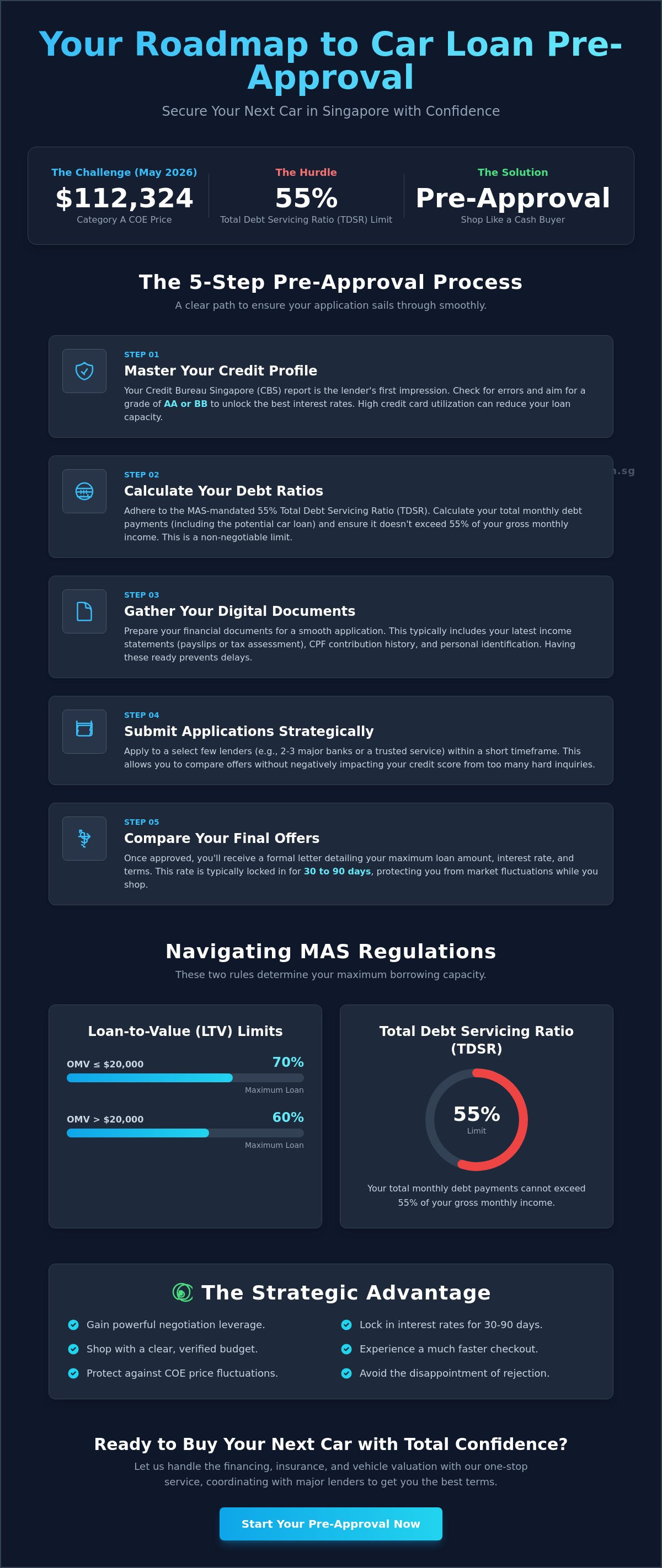

With Category A COE prices sitting at $112,324 as of May 2026, walking into a showroom without a financial shield is a gamble most Singaporeans can't afford to take. You've likely felt a pang of anxiety while browsing the latest BYD or Tesla models, wondering if your application will actually clear the strict 55% Total Debt Servicing Ratio (TDSR) limit. It's a common fear to find the perfect vehicle only to face a sudden rejection or a lower loan-to-value limit than you expected.

Understanding how to get pre approved for a car loan is the most strategic move you can make before you ever step onto a dealership floor. It transforms you from a hopeful browser into a serious buyer with real negotiation leverage. We'll help you master this process so you can secure the best interest rates, whether you're eyeing a brand new EV or a reliable pre-owned car. This guide provides a clear roadmap through MAS regulations and current bank rates to ensure you buy your next vehicle with total confidence and a faster checkout process.

Key Takeaways

- Master the essential steps on how to get pre approved for a car loan to lock in competitive interest rates and gain negotiation leverage.

- Understand how MAS regulations, including LTV limits and TDSR requirements, determine your maximum borrowing capacity for new or pre-owned vehicles.

- Compare the advantages of traditional bank loans versus in-house dealer financing to find the most suitable option for your credit profile.

- Learn how to prepare your Credit Bureau Singapore report and financial documents to ensure a smooth, rejection-free application process.

- Discover the benefits of a one-stop service that coordinates with major lenders to manage your financing, insurance, and vehicle valuation.

What is Car Loan Pre-Approval and Why is it Essential in Singapore?

In the Singaporean automotive market, a car loan pre-approval is more than just a piece of paperwork. It is a formal document from a bank or lender that specifies the maximum amount you are eligible to borrow based on a rigorous credit assessment. Unlike a simple verbal estimate, this is a conditional commitment. To understand the global standard for this process, you can read more about What is Pre-Approval? and how it functions as a primary step in major financial transactions. Knowing how to get pre approved for a car loan allows you to shop with a verified budget. This is vital given that car prices in 2026 are heavily influenced by six-figure COE premiums and shifting MAS regulations.

A key benefit of this process is that it typically locks in an interest rate for a period of 30 to 90 days. This protection is invaluable. While you are browsing brand new cars or searching for the right pre-owned vehicle, you don't have to worry about sudden interest rate hikes. You should also distinguish this from pre-qualification. Pre-qualification is a surface-level look at your finances; pre-approval involves a deep dive into your Credit Bureau Singapore (CBS) report and income documents.

To better understand this concept, watch this helpful video:

The Strategic Advantage of Being Pre-Approved

Securing a pre-approval changes your entire approach at the dealership. Instead of being a "monthly payment buyer" who might be swayed by long-term loan tenures that hide the total cost, you become a "total price buyer." You know exactly what you can afford. This clarity speeds up the Land Transport Authority (LTA) registration process because the financing is already lined up. It simplifies the administrative work for both you and the seller. Most importantly, it prevents the emotional letdown of finding a car you love only to have your loan application rejected after you have already signed the sales agreement and paid a deposit.

How Pre-Approval Protects You Against COE Fluctuations

With Category A COE prices reaching $112,324 in May 2026, the total cost of a car can shift overnight. Because your loan amount is tied to the total purchase price, a spike in COE can push you beyond your borrowing limit. By learning how to get pre approved for a car loan early, you establish a hard ceiling for your budget. You will know exactly how much of a COE increase you can absorb before the vehicle becomes unaffordable. This foresight is essential for managing the high total cost of ownership in Singapore's current market. It ensures you stay within the 55% Total Debt Servicing Ratio (TDSR) regardless of market volatility.

The 5-Step Process to Get Pre-Approved for an Auto Loan

Securing a financial head start requires a systematic approach. In 2026, the process is more digitized and transparent than ever before. By following a structured path, you can ensure your application aligns with MAS Regulations on Car Loans, which dictate strict borrowing limits based on a vehicle's Open Market Value (OMV). Learning how to get pre approved for a car loan involves five clear steps: reviewing your credit, calculating your debt ratios, gathering digital data, submitting applications strategically, and comparing your final offers.

Step 1: Mastering Your Credit Profile

Your Credit Bureau Singapore (CBS) report is the first thing a lender examines. Major Singaporean banks typically prefer a credit grade of AA or BB. These grades signal that you're a low-risk borrower, which often unlocks the most competitive interest rates. Before you apply, pull your own report to check for inaccuracies. Even a small error in your repayment history can lead to a lower loan-to-value (LTV) limit or a flat rejection. You should also look at your existing credit card debt. High utilization on your cards can reduce your total car loan capacity, even if you pay your bills on time every month.

Step 2: Digital Documentation and MyInfo

The days of printing stacks of payslips are over. You can now use Singpass to automate the submission of your income and CPF contribution history. For salaried employees, this usually covers the last 12 months of data. Self-employed individuals may need to provide two years of Notice of Assessment (NOA) records. Digital integration via MyInfo reduces approval time to minutes in 2026. This efficiency allows you to focus on finding the right vehicle rather than chasing paperwork. If you're ready to see what's available, browse our curated selection of pre-owned cars.

The remaining steps of the process ensure you stay within legal limits while getting the best deal:

- Calculate your TDSR: Ensure your total monthly debt repayments, including the new car loan, don't exceed 55% of your gross monthly income.

- Submit applications strategically: Apply to multiple lenders within a 14-day window. This prevents multiple "hard inquiries" from negatively impacting your credit score.

- Compare IPA letters: Once you receive your In-Principle Approval (IPA) letters, look beyond the monthly payment. Compare the interest rates, which for bank loans in early 2026 range from 2.48% to 3.08%, and check for any early settlement penalties.

By completing these steps, you verify your eligibility for the maximum loan tenure of 7 years. You'll also know if you qualify for the 70% LTV limit for cars with an OMV of $20,000 or less, or the 60% limit for higher-value models. This preparation is the key to how to get pre approved for a car loan with minimal stress.

Comparing Lenders: Banks vs. In-House Dealer Financing

Choosing the right lender is just as critical as finding the right car. When you're researching how to get pre approved for a car loan, you'll encounter three main paths: traditional banks, in-house financing, and finance companies. Each serves a different profile. All of them must operate within the MAS regulations on car loans. These rules ensure that your total borrowing stays within sustainable limits based on the car's Open Market Value and your monthly income.

Traditional banks like DBS, UOB, and OCBC offer the lowest interest rates. These typically range from 2.48% to 3.08% as of early 2026. However, they have the strictest criteria. If you have a stable salary and a high credit score, a bank is your best bet. Finance companies provide a middle-ground option. They're particularly popular for buyers of commercial vehicles who need slightly more flexible terms than a standard consumer bank loan.

When to Choose a Bank Loan

Bank loans are ideal for buyers with a clear financial history and consistent CPF contributions. When comparing bank offers, look at the Effective Interest Rate (EIR) instead of just the flat rate. The EIR accounts for the reducing balance of your loan and reflects the true cost of borrowing. If you're looking at brand new cars, you'll often find special promotional rates tied to specific bank partners. These deals can significantly lower your total cost of ownership over a 7-year tenure.

The Benefits of Dealer In-House Financing

In-house financing offers a vital alternative for those who don't fit the traditional banking mold. This includes self-employed individuals, commission-based earners, or those with "thin" credit files. Approval rates are generally higher because the dealership has more flexibility in assessing risk. You can often bundle insurance and road tax into one monthly payment. This simplifies your budgeting. This route also provides faster processing times, especially for used cars already in the dealer's inventory. While interest rates are higher, starting from 3.50% to 4.28%, the convenience and accessibility are significant advantages.

Always watch for hidden costs that can inflate your loan. Common fees include:

- Processing Fees: Upfront administrative charges for setting up the loan.

- Early Settlement Penalties: Fees charged if you pay off the loan before the tenure ends.

- Unpaid Interest Charges: Costs associated with late payments.

Understanding these nuances is a key part of how to get pre approved for a car loan without any surprises later on. By comparing these options early, you'll enter the showroom with a clear financial strategy. This ensures you aren't just buying a car, but also securing a sustainable financial commitment.

Navigating MAS Regulations: LTV Limits and TDSR

Understanding the rules set by the Monetary Authority of Singapore is essential when learning how to get pre approved for a car loan. These regulations aren't just guidelines. They're legal requirements that every bank and licensed lender must follow. They ensure that car buyers don't overextend themselves financially in a market where vehicle costs are high. By knowing these limits upfront, you can avoid the frustration of a rejected application and focus on cars within your actual reach.

Calculating Your Required Down Payment

Your required down payment depends entirely on the Open Market Value (OMV) of the vehicle. If the OMV is $20,000 or less, you can borrow up to 70% of the purchase price. This means you need a 30% down payment. For cars with an OMV above $20,000, the maximum loan drops to 60%. Consequently, you must prepare a 40% down payment. These limits are non-negotiable under MAS law. Whether you're buying brand new cars or a second-hand model, the bank cannot exceed these ceilings regardless of your income level.

Understanding the 55% TDSR Rule

The Total Debt Servicing Ratio (TDSR) is perhaps the most critical hurdle in the pre-approval process. It caps your total monthly debt repayments at 55% of your gross monthly income. This includes your mortgage, personal loans, credit card balances, and the prospective car loan. If your existing debts are high, your car loan amount might be restricted even if the LTV allows for more. For example, a high mortgage payment could eat up a large portion of your 55% allowance, leaving less room for your vehicle financing.

To improve your chances, consider clearing small debts or closing unused credit lines before you apply. Paying off a lingering renovation loan or a credit card balance can significantly lower your TDSR. If you're eyeing a high-priced continental car, a joint application with a spouse can help. Combining incomes often makes it easier to stay under the 55% threshold. Knowing these numbers helps you determine how to get pre approved for a car loan that fits your actual budget without straining your monthly cash flow.

Finally, remember that the maximum loan tenure in Singapore is strictly capped at 7 years. This applies to all motor vehicle loans, including those for pre-owned vehicles. Shorter tenures result in higher monthly payments but lower total interest costs over time. If you need help navigating these complex rules, consult our experienced team to find a vehicle that matches your financial profile and meets all regulatory requirements.

Finalizing Your Purchase with Carz World Pte Ltd

Once you've mastered the steps of how to get pre approved for a car loan, the final stage is finding a partner who can turn that paperwork into a set of keys. Carz World Pte Ltd operates as a comprehensive hub for your automotive needs. We work closely with all major banks in Singapore to help you secure the most favorable pre-approval terms. This collaborative approach ensures that you aren't just getting a generic loan, but a financial package tailored to your specific TDSR and income profile. Our team acts as a bridge between you and the lenders, ensuring all requirements are met before you commit to a purchase.

Our service model is built on transparency. In an industry where hidden admin fees or agreement fees can often surprise buyers at the last minute, Carz World Pte Ltd maintains a clear and honest pricing structure. You'll receive expert guidance on COE bidding strategies and the management of complex LTA paperwork. This level of support is designed to make the transition from a loan applicant to a car owner as fluid as possible. We focus on making the logistical process feel like a seamless experience, allowing you to focus on the excitement of your new vehicle.

From Pre-Approval to Drive-Away

The real advantage of our process is how we match your pre-approved budget to our pre-owned car collection. We ensure that the vehicle you choose fits perfectly within the LTV limits we discussed earlier. If you have an existing vehicle, our trade-in service allows you to sell your car and use the proceeds to offset your required down payment. This is a strategic way to manage the 40% upfront cost required for cars with an OMV above $20,000. Our commitment to professional, customer-centric service is reflected in our extensive library of client testimonials, where our staff members are frequently praised for their dedication and attention to detail.

Ready to Start Your Journey?

Navigating the 2026 car market requires more than just a search engine. It requires local expertise and a methodical approach. We invite you to visit our showrooms at Ubi or Alexandra for a personalized consultation with Carz World Pte Ltd. Our experienced staff will handle the TDSR and MAS calculations for you, taking the guesswork out of how to get pre approved for a car loan. We'll help you navigate Category A or Category B COE fluctuations with ease and ensure your financing is secured at the best possible rates.

Take the first step toward your next vehicle with total confidence. Get a personalized car loan consultation today and experience a seamless, organized transaction from start to finish.

Drive Away with Absolute Confidence

Mastering the details of MAS regulations and debt ratios puts you in the driver's seat before you even start the engine. You now understand how your OMV dictates your down payment and why the 55% TDSR threshold is a non-negotiable part of the Singaporean lending landscape. By learning how to get pre approved for a car loan, you've moved past the uncertainty of rejection and gained the leverage needed to shop with total clarity.

As a trusted parallel importer and pre-owned specialist, we're here to ensure your transition from applicant to owner is seamless. We provide transparent, MAS-compliant financing options that protect your interests and fit your lifestyle. Whether you're visiting our convenient showrooms at Ubi or Alexandra, our team is ready to help you navigate the final steps of your journey.

Don't let market volatility or complex paperwork slow you down. Secure Your Pre-Approval and Browse Our Inventory today. We look forward to helping you find the perfect vehicle with a financial plan that works for you.

Frequently Asked Questions

Does a car loan pre-approval guarantee I will get the loan?

No, a pre-approval is a conditional offer rather than a final guarantee. Lenders perform a final verification of your financial status before disbursement to ensure your income, employment, and debt levels haven't changed since the initial application. Any major shifts in your financial profile or a change in the vehicle's valuation could lead to a revision of the loan terms or a withdrawal of the offer.

How long does a car loan pre-approval last in Singapore?

Most pre-approvals in Singapore are valid for a period of 30 to 90 days. This timeframe is designed to give you enough room to browse various showrooms and participate in at least two COE bidding cycles. If you don't select a vehicle and finalize the purchase within this window, you'll likely need to re-submit your latest income documents for a fresh credit assessment.

Will getting pre-approved for a car loan hurt my credit score?

A single pre-approval application involves a "hard inquiry," which may cause a minor and temporary dip in your credit score. However, Credit Bureau Singapore recognizes that buyers often compare rates. If you submit multiple applications within a 14-day window, the bureau typically treats them as a single inquiry. This prevents your score from being significantly impacted while you search for the best terms.

Can I use a pre-approval for both new and used cars?

Yes, you can use a pre-approval for both types, but the final loan amount will adjust based on the vehicle's age and Open Market Value. Banks often apply different interest rates for new versus pre-owned vehicles. Understanding how to get pre approved for a car loan allows you to see these specific rate variations early, helping you decide which car category fits your budget best.

What is the difference between flat rate and effective interest rate (EIR)?

The flat rate calculates interest based on the original loan amount for the entire tenure, while the EIR reflects the true cost by accounting for the reducing principal balance. In Singapore, the EIR is always higher than the flat rate. It's the most accurate metric for comparing different loan offers because it shows the actual interest you pay as you settle your debt over time.

Can I get pre-approved if I am an expat living in Singapore?

Yes, expats can get pre-approved provided they meet the typical minimum monthly income requirement of $4,000 and hold a valid Employment Pass. Most lenders require your pass to be valid for at least six months beyond the date of your application. Some banks may also request a higher down payment or a local guarantor depending on the length of your residency.

What happens if the car price changes after I get pre-approved?

If the car price increases, your loan remains capped at the pre-approved limit or the MAS LTV ceiling, whichever is lower. You'll need to cover any price gap with a larger cash down payment. If the price drops, the bank will simply reduce the loan amount proportionally. This ensures the total financing stays within the mandatory 60% or 70% loan-to-value limits.

Do I need to have a specific car in mind before applying for pre-approval?

No, you don't need a specific vehicle to begin the process of how to get pre approved for a car loan. Most savvy buyers get pre-approved for a maximum budget first. This strategy allows you to shop with total confidence, knowing exactly which price range and COE category you can afford without the risk of a loan rejection after you've found a car.

In Same Category

- How to Get a Fair Trade-In Offer for Your Car in Singapore: 2026 Guide

- Selling a Car with an Outstanding Loan in Singapore: The 2026 Complete Guide

- Car Consignment vs Direct Sale in Singapore: The 2026 Seller’s Guide

- How to Avoid Overpaying for a Used Car in Singapore (2026 Guide)

- 15 Practical Saving Tips for Car Buyers in Singapore (2026 Edition)

Related by Tags

- How to Get a Fair Trade-In Offer for Your Car in Singapore: 2026 Guide

- Selling a Car with an Outstanding Loan in Singapore: The 2026 Complete Guide

- Car Consignment vs Direct Sale in Singapore: The 2026 Seller’s Guide

- How to Avoid Overpaying for a Used Car in Singapore (2026 Guide)

- 15 Practical Saving Tips for Car Buyers in Singapore (2026 Edition)

- Total Cost of Ownership Calculator: The Real Cost of a Car in Singapore (2026)

- When to Replace Your Car in Singapore: The 2026 Strategic Guide

- Used Car Warranty in Singapore: The Ultimate Guide to Protecting Your Investment (2026)

- Pre-Purchase Car Inspection Singapore: The Complete Buyer’s Guide (2026)

- Used Car Maintenance Costs in Singapore 2026: The Complete Owner’s Guide

- Buying Chinese Cars in Singapore: The Ultimate 2026 Buying Guide

- Common Problems with Used Cars: A Singapore Buyer’s Guide to Avoiding Lemons

- The Importance of Car Service History: Protecting Your Investment in 2026

- Financial Planning for Buying a Car in Singapore: A 2026 Roadmap

- Government Regulations for Car Ownership in SG: The 2026 Essential Guide

- Top-of-the-Chart Hybrid Cars in Singapore: The 2026 Buyer’s Guide

- The Impact of COE on Used Car Prices in Singapore: A 2026 Guide

- Used Car Market Outlook Singapore 2026: Trends, COE Impact, and Value Shifts

- Refinancing a Car Loan in Singapore: The Complete 2026 Strategy Guide

- COE for Commercial Vehicles: The Complete 2026 Guide for Singapore Businesses

- Electric Cars (EV) in Singapore: The Ultimate 2026 Buying Guide

- Performance Cars for Sale in Singapore: The Enthusiast’s 2026 Buying Guide

- Best Compact SUV for City Driving in Singapore: The 2026 Urban Guide

- Used Japanese Cars for Sale: The Ultimate Singapore Buyer’s Guide for 2026

- Best 7 Seater SUV Singapore: The 2026 Family Guide to Space and Value

- Bidding for COE Number in 2026: The Complete Strategic Guide for Singapore Car Buyers

- Cat A vs Cat B COE Difference: The Complete 2026 Singapore Guide

- COE Price Trend Analysis 2026: Is Now the Best Time to Buy a Car in Singapore?

- What Affects Car Resale Value in Singapore? A 2026 Guide to Maximising Your Return

- Car Valuation Certificate in Singapore: Your Complete Guide to Official Vehicle Worth

- Selling a Car with an Outstanding Loan in Singapore: The 2026 Complete Guide

- Detailing Your Car for Higher Resale Value: The Ultimate Singapore Guide for 2026

- When to Sell Your Car in Singapore: The Strategic 2026 Guide to Maximizing Returns

- Car Dealership Financing vs Bank Loan in Singapore: The 2026 Comparison Guide

- Common Problems with Used Cars: The Singapore Buyer’s Guide to Avoiding Lemons

- The Master Used Car Inspection Checklist for Singapore (2026 Edition)

- Deregistering a Car for Export in Singapore: The 2026 Complete Guide