Car Loan Early Settlement Penalty in Singapore: The Complete 2026 Guide

Why is your car loan redemption amount significantly higher than the remaining principal on your statement? It's a question that catches many Singaporean drivers off guard when they prepare to sell or trade in their vehicles. You've likely felt that sting of frustration when realizing your car loan early settlement penalty isn't just a simple flat fee. It's natural to feel confused by the complex math banks use to protect their interest earnings, especially when the numbers don't seem to add up in your favor.

This guide will help you master the "Rule of 78" and calculate exactly what you'll pay or save by settling early in 2026. We'll break down specific bank penalties, such as the 1% charges at DBS and OCBC or the 1.5% fee at UOB, along with the standard 20% interest rebate charge. By the end of this article, you'll have a clear dollar-value understanding of your costs. This knowledge ensures you can make a confident decision on whether to settle now or wait, allowing for a smooth transition when you're ready to explore our range of pre-owned or brand new cars.

Key Takeaways

- Understand why Singaporean banks charge early redemption fees and the specific administrative costs involved in closing your loan.

- Demystify the "Rule of 78" to see exactly how interest is weighted toward the start of your loan term.

- Identify the most strategic time to sell by calculating your car loan early settlement penalty against current 2026 COE prices.

- Learn the exact steps to request an official full settlement quote from major lenders like DBS, OCBC, and UOB.

- Discover how a professional trade-in process can handle your outstanding loan balance while maximizing your remaining equity.

Understanding the Car Loan Early Settlement Penalty in Singapore

In Singapore, early redemption refers to the process of paying off your vehicle loan before the agreed-upon tenure finishes. Whether you are upgrading to one of our brand new cars or simply have extra cash from a year-end windfall, you'll encounter a car loan early settlement penalty. This cost is a protective measure for financial institutions. Banks impose these charges to recover administrative costs, lost future interest, and the commissions they paid to car dealers at the start of the loan agreement.

The legal framework for these transactions is primarily governed by the Hire Purchase Act. This act outlines the rights and obligations of both the lender and the borrower. It provides a specific structure for the statutory rebate of interest, ensuring that consumers aren't unfairly charged. However, the act still allows banks to apply specific fees to ensure their business remains viable when a contract is ended prematurely. Understanding these rules helps you time your car sale or trade-in effectively.

To better understand how these costs affect your financial planning, watch this helpful video:

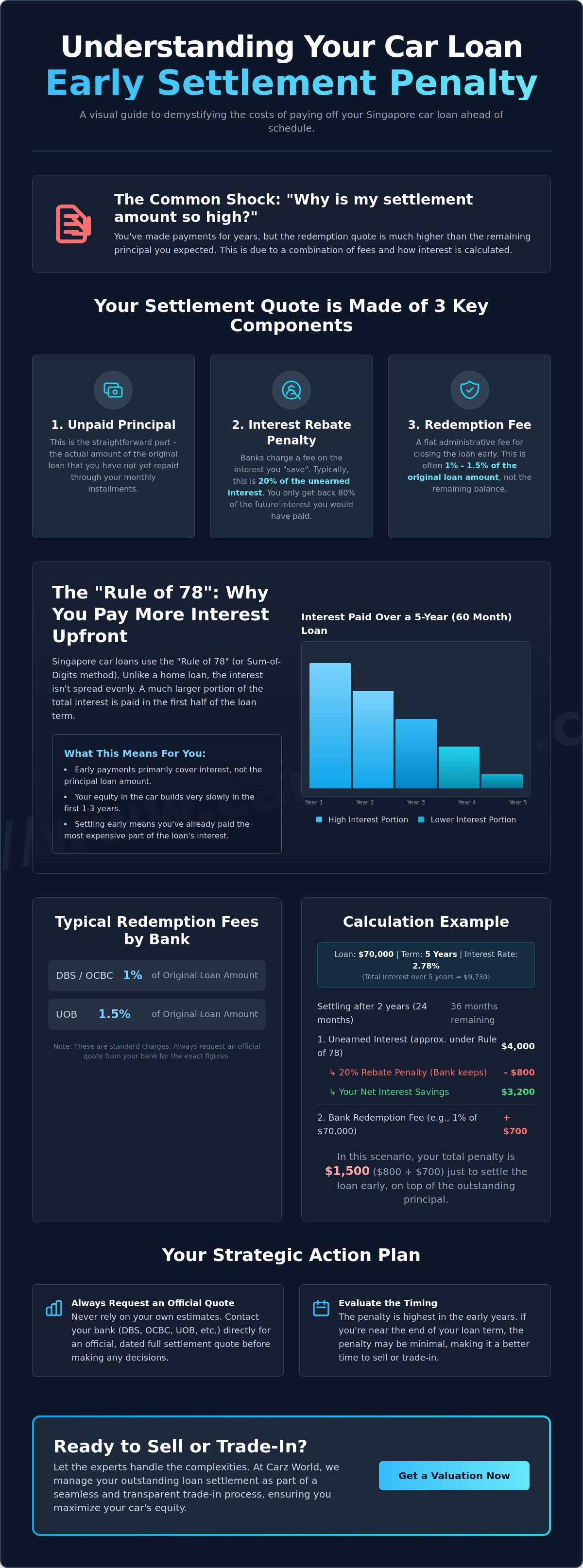

The Three Components of the Settlement Cost

Your final payout figure is not just your remaining balance. It consists of three specific parts. First is the unpaid principal, which is the actual amount you borrowed that hasn't been repaid yet. Next is the interest rebate penalty. Banks use The Rule of 78 to calculate how much interest you save by paying early. However, they typically charge a fee of 20% on that rebate amount. This means you only receive 80% of the potential interest savings. Finally, most banks add a redemption fee, which is often 1% of the original financed amount. These fees can add up to several thousand dollars depending on your loan size.

Why "Simple Interest" is a Misconception

Many drivers assume car loans work like home loans with a reducing balance. This is not the case. Singapore car loans utilize "add-on" interest. This means the interest is calculated on the full principal for the entire loan period right at the beginning. Because of this structure, car loans are front-loaded with interest charges. You pay off the interest much faster than the principal in the early years of the tenure. Consequently, your car loan early settlement penalty might feel surprisingly high if you try to settle within the first two or three years. The redemption amount often stays high even as you make regular monthly payments.

The Rule of 78: How the Penalty is Calculated

The financial impact of a car loan early settlement penalty is rarely a simple calculation. Banks in Singapore utilize the "Rule of 78," also known as the Sum of Digits method, to determine how much interest you've technically "earned" versus what you still owe. This system isn't linear. It's designed to weight interest payments heavily toward the beginning of your loan term. If you look at a seven-year loan, you'll find that you've paid off a significant portion of the total interest within the first 24 months, even if the principal balance remains high.

This front-loading creates a curve where your equity in the vehicle grows slowly at first. When you request a redemption, the bank calculates the "unearned interest" for the remaining months. However, standard bank practice dictates that they don't return the full amount. Instead, they apply a "20% Rebate Penalty." This means you only receive 80% of the unearned interest back. The remaining 20% is kept by the bank as a fee for the early termination of the contract. You can see a detailed breakdown of how banks calculate the settlement quote to see these percentages in action.

A Step-by-Step Calculation Example

Consider a $70,000 loan taken over five years at an interest rate of 2.78%. The total interest for the full term would be $9,730. If you decide to settle the loan at the two-year mark, you might expect to save 60% of that interest. Under the Rule of 78, the "unearned interest" for the remaining three years is actually much lower than a simple pro-rata split. If the calculated unearned interest is $4,000, the bank applies the 80% rebate rule. You'd only receive a credit of $3,200. The "hidden cost" here is the $800 the bank retains from your potential interest savings.

The 1% Principal Penalty

In addition to the interest rebate loss, most Singaporean lenders charge a flat fee based on the original loan amount. For DBS and OCBC, this is typically 1% of the total sum you first borrowed. For a $70,000 loan, that's an immediate $700 charge. UOB often applies a slightly higher rate of 1.5%. It's a common point of confusion for many drivers. They expect the penalty to be based on the *outstanding* balance, but it's almost always calculated from the *original* financed amount. These fees are rarely waived unless you're performing an internal refinancing, though administrative fees ranging from $200 to $800 can sometimes be negotiated during a trade-in.

Gaining a clear picture of your car loan early settlement penalty allows you to plan your next vehicle upgrade more effectively. If you're curious about how your current loan balance affects your next purchase, you can browse our latest inventory of quality vehicles to see what fits your updated budget.

Strategic Timing: When is Early Settlement Worth It?

Timing is everything when managing a vehicle's lifecycle in Singapore. Many drivers believe in the "Halfway Mark" myth. They assume the 50% point of a loan term is the ideal time to settle. This logic fails because of the interest front-loading we've previously discussed. By the time you reach the middle of a 7-year tenure, you've already paid nearly 70% of the total interest. Settling at this stage often means you're paying a car loan early settlement penalty for very little interest rebate in return. The cost of the penalty might actually outweigh the interest you'd save over the remaining months.

Strategic timing requires a look at the opportunity cost. If you keep a high-interest loan while having the cash to settle it, you're effectively losing money every month. However, if that cash could earn a higher return in a low-risk investment, waiting might be better. You must compare the typical 1% to 3% penalty against the potential interest savings. Since COE renewal loan interest rates in 2026 can exceed 4%, settling a lower-interest car loan early just to take a new, more expensive loan for a different car may not always be the smartest move.

The Breakeven Analysis

A successful settlement strategy relies on understanding your equity position. You have positive equity when your car's resale value exceeds the total settlement amount. Conversely, negative equity, or being "underwater," occurs when you owe the bank more than the car is worth. If you're in a negative equity position, settling early requires you to pay the difference out of pocket. This is often the case in the first two years of a loan when depreciation is steepest. The breakeven point usually occurs when the interest you'll save by settling finally exceeds the sum of the car loan early settlement penalty and any administrative fees, which typically range from $200 to $800.

The Impact of High COE on Settlement Strategy

The 2026 COE landscape plays a massive role in this decision. High COE prices have significantly pushed up the resale value of older cars. If you bought your car when COE was lower, your vehicle might now command a premium that completely offsets the settlement fees. This creates a unique window to exit your current loan and sell your car without incurring a net loss. Always check the current Prevalent Quota Premium (PQP) trends before requesting your final quote. A rising PQP often makes your current car more valuable to buyers looking to avoid the high costs of brand new registrations.

How to Request a Full Settlement Quote from Your Bank

Obtaining a formal quotation is the only way to see the final impact of your car loan early settlement penalty. You shouldn't rely solely on mobile app estimations or verbal guesses. These figures often lack the precise breakdown of administrative fees or the exact "Valid Until" date required for a clean transaction. To start, locate your Hire Purchase agreement or your latest loan statement to find your specific account number. This ensures the bank's car loan department identifies the correct facility immediately.

Most major lenders in Singapore, including DBS, OCBC, and UOB, require a written request or a call to their dedicated auto-loan hotlines. When you contact them, specifically ask for a "Full Settlement Quote." This document is essential because it freezes your balance for a set period, usually 7 to 14 days. It provides a clear roadmap of your liabilities, allowing you to verify the bank's math against the Rule of 78 logic we explored earlier. Without this formal paper, you risk underpaying and incurring late fees that could further complicate your vehicle sale.

The process usually involves these key steps:

- Identify your loan account number and Hire Purchase agreement.

- Contact the bank's car loan department (DBS, OCBC, UOB, etc.).

- Request a "Full Settlement Quote" with a specific "Valid Until" date.

- Review the breakdown of principal, rebate, and fees.

- Verify the figure against your own Rule of 78 estimate.

Documents You Will Need

Banks require specific identifiers to release sensitive financial data. You'll need your NRIC or Passport and your vehicle registration number ready. Most importantly, you must have your LTA Log Card. This document verifies ownership details and the current financing status of the vehicle. In 2026, you can quickly download this via the LTA e-service portal using your Singpass login. Having these documents prepared ensures the bank can process your request without unnecessary back-and-forth delays.

What to Look for in the Quote

Once you receive the document, don't just look at the final total. Examine the line-by-line breakdown. Most Singaporean banks require a 30-business-day notice period for early redemption. If you want to settle immediately, the quote will include a charge for "interest in lieu of notice," which is typically one month of interest. You should also check the following items:

- Interest Rebate: Verify that the rebate follows the standard 80% industry practice.

- Administrative Fees: Look for processing charges, which typically range from $200 to $800.

- Principal Balance: Ensure the outstanding principal matches your own payment records.

If you find a discrepancy in the principal balance or if the fees seem higher than your original contract, ask for a detailed calculation sheet. Banks are generally methodical, but errors can occur during manual entries. Providing your own payment history can help resolve these issues quickly. If the calculation of your car loan early settlement penalty feels overwhelming, our team can assist. We ensure all figures are accurate before finalizing your trade-in equity when you partner with Carz World.

Selling or Trading In? How Carz World Handles Your Loan

When you decide to move on from your current vehicle, the logistical hurdle of closing your bank account can feel daunting. At Carz World, we provide a seamless trade-in process designed to remove the stress of dealing with financial institutions. We take over the responsibility of settling your outstanding loan directly with the bank. This ensures that you don't have to manage multiple phone calls or paperwork submissions yourself. Our team coordinates with lenders like DBS, OCBC, and UOB to ensure the redemption is handled accurately and promptly.

We calculate your "Trade-In Equity" by taking the agreed resale value of your car and subtracting the full settlement amount. This figure naturally includes the car loan early settlement penalty and any related administrative costs. By having a clear understanding of these numbers, you can see exactly how much cash you have available for your next move. You might choose a direct trade-in for maximum convenience, or you may prefer selling your car through consignment to potentially achieve a higher price. Regardless of your choice, our priority is to protect your interests and ensure a clean title transfer.

Trust is a critical factor in this process. Some "fly-by-night" dealers may delay settling your bank loan after taking possession of your car, which can lead to late interest charges or credit score damage. We pride ourselves on our long-term reputation and methodical approach. We provide immediate confirmation once the bank loan is fully settled. This transparency gives you the confidence that your financial obligations are completely resolved before you drive away in your next vehicle.

Transparency in Valuation

Our commitment to professional service starts with a straightforward appraisal. You can visit our dedicated showrooms at Ubi or Alexandra for a detailed assessment. Our pre-owned car expertise allows us to offer fair, market-reflective prices that help cover your loan liabilities. You'll work with dedicated consultants who take the time to explain the valuation. This personalized attention ensures you aren't just another transaction; you're a valued partner in a transparent process.

Upgrading to Your Next Vehicle

Once your current loan is settled, you can apply any positive equity toward a brand new car or a premium used model from our inventory. Our team also assists in structuring your next loan. We help you choose terms that balance monthly affordability with the flexibility to settle early in the future without excessive car loan early settlement penalty costs. We believe in making complex logistical processes feel like a seamless experience. Get a professional valuation and loan consultation at Carz World today.

Take Control of Your Car Loan Settlement

Mastering the math behind the Rule of 78 is the first step toward a smarter vehicle upgrade. You now know that timing your sale to align with positive equity and high COE values can significantly reduce the impact of a car loan early settlement penalty. By requesting a formal quote and verifying the interest rebate, you ensure no hidden fees eat into your savings. These steps provide the clarity needed to decide whether to settle now or wait for a better market window.

Carz World has served as a trusted parallel importer and pre-owned specialist since our inception. Our transparent settlement process removes the guesswork. We don't charge hidden dealership admin fees. Our dedicated consultants are frequently highlighted in over 500+ positive reviews for their individual, high-quality service. We handle the complex bank communications so you can focus on finding your next vehicle.

Sell your car with confidence; get a free valuation and loan check at Carz World today. We look forward to making your next automotive transition smooth and rewarding.

Frequently Asked Questions

What is the standard early settlement penalty for car loans in Singapore?

The standard car loan early settlement penalty typically involves a fee of 1% of the original loan amount. For example, DBS and OCBC apply this 1% charge, while UOB generally charges 1.5%. In addition to this principal based fee, banks also charge a 20% penalty on the interest rebate calculated under the Rule of 78. You should also expect administrative fees ranging from $200 to $800 depending on the lender.

Can I negotiate the 20% interest rebate penalty with my bank?

Negotiating the 20% interest rebate penalty is difficult because it's a standard clause in most Singaporean Hire Purchase agreements. Banks view this as a non-negotiable cost to recover lost future earnings. While the rebate penalty itself is fixed, you may have better luck negotiating the administrative processing fees. This is especially true if you're a long-term premier banking customer or if you're working with a reputable dealer during a trade-in.

Is it always better to pay off my car loan early if I have the cash?

It's not always financially beneficial to settle early, especially if you're in the final years of your loan tenure. Because interest is front-loaded, the interest you save in the last 12 to 24 months might be less than the car loan early settlement penalty. You should calculate the total savings against the penalty fees. If the penalty exceeds the remaining interest, it's often better to continue with your monthly instalments.

How does the Rule of 78 affect my car’s resale value?

The Rule of 78 doesn't change the market value of your car, but it significantly impacts your net proceeds after a sale. This formula ensures that your outstanding loan balance decreases slowly in the early years. When you sell your car, a larger portion of the sale price goes toward settling the bank debt rather than into your pocket. This often results in lower "Trade-In Equity" than many owners expect during the first half of their loan term.

What happens to my car insurance when I settle my loan early?

Your car insurance remains valid, but you must update the policy details once the bank releases its interest in the vehicle. You'll need to inform your insurer to remove the bank's name as the "loss payee" or "hire purchase" interest holder. Once this is updated, any future insurance payouts for claims will be made directly to you. This step is crucial for ensuring you have full control over your vehicle's financial assets.

How long does the bank take to process a full settlement in 2026?

Banks in Singapore typically require a 30-business-day written notice for a full settlement. If you need to settle immediately, you'll usually be charged one month's interest in lieu of that notice. Once the payment is received, the bank takes approximately 7 to 14 working days to update the LTA system. This update officially clears the financing record, allowing for a smooth transfer of ownership to a new buyer or dealer.

Can I settle my car loan early if I am selling the car to a private buyer?

Yes, you can settle early during a private sale, but the process requires careful coordination. The buyer or their financier must pay the settlement amount directly to your bank to discharge the loan. Ownership transfer through the LTA e-service cannot be completed until your bank has updated the status to show the loan is fully paid. It's often helpful to have a formal settlement quote ready to show the buyer exactly what's owed.

Will settling my car loan early improve my credit score in Singapore?

Settling your loan early reflects as a "closed" account in your Credit Bureau Singapore (CBS) report, which is generally positive. It shows you have the financial capacity to clear your debts ahead of schedule. However, it doesn't provide a massive instant boost to your score. Maintaining a consistent history of on-time monthly payments is actually more influential for your long-term creditworthiness than a single early redemption event.

In Same Category

- How to Negotiate Used Car Price in Singapore: The 2026 Insider’s Guide

- How to Sell Your Car in Singapore: The 2026 Ultimate Guide to Getting Top Dollar

- Checking for Accident Damage on a Car: The Ultimate 2026 Singapore Inspection Guide

- 10 Critical Red Flags to Watch for When Buying a Used Car in Singapore (2026)

- Parallel Import New Cars Singapore: The 2026 Ultimate Buying Guide

Related by Tags

- Checking for Accident Damage on a Car: The Ultimate 2026 Singapore Inspection Guide

- Parallel Import New Cars Singapore: The 2026 Ultimate Buying Guide

- How to Get a Fair Trade-In Offer for Your Car in Singapore: 2026 Guide

- Selling a Car with an Outstanding Loan in Singapore: The 2026 Complete Guide

- Car Consignment vs Direct Sale in Singapore: The 2026 Seller’s Guide

- How to Avoid Overpaying for a Used Car in Singapore (2026 Guide)

- 15 Practical Saving Tips for Car Buyers in Singapore (2026 Edition)

- When to Replace Your Car in Singapore: The 2026 Strategic Guide

- Used Car Warranty in Singapore: The Ultimate Guide to Protecting Your Investment (2026)

- Buying Chinese Cars in Singapore: The Ultimate 2026 Buying Guide

- Common Problems with Used Cars: A Singapore Buyer’s Guide to Avoiding Lemons

- The Importance of Car Service History: Protecting Your Investment in 2026

- Financial Planning for Buying a Car in Singapore: A 2026 Roadmap

- Government Regulations for Car Ownership in SG: The 2026 Essential Guide

- Top-of-the-Chart Hybrid Cars in Singapore: The 2026 Buyer’s Guide

- The Impact of COE on Used Car Prices in Singapore: A 2026 Guide

- Used Car Market Outlook Singapore 2026: Trends, COE Impact, and Value Shifts

- Refinancing a Car Loan in Singapore: The Complete 2026 Strategy Guide

- COE for Commercial Vehicles: The Complete 2026 Guide for Singapore Businesses

- Performance Cars for Sale in Singapore: The Enthusiast’s 2026 Buying Guide

- Best Compact SUV for City Driving in Singapore: The 2026 Urban Guide

- Used Japanese Cars for Sale: The Ultimate Singapore Buyer’s Guide for 2026

- Best 7 Seater SUV Singapore: The 2026 Family Guide to Space and Value

- Bidding for COE Number in 2026: The Complete Strategic Guide for Singapore Car Buyers

- Cat A vs Cat B COE Difference: The Complete 2026 Singapore Guide

- COE Price Trend Analysis 2026: Is Now the Best Time to Buy a Car in Singapore?

- What Affects Car Resale Value in Singapore? A 2026 Guide to Maximising Your Return

- Car Valuation Certificate in Singapore: Your Complete Guide to Official Vehicle Worth

- Selling a Car with an Outstanding Loan in Singapore: The 2026 Complete Guide

- Detailing Your Car for Higher Resale Value: The Ultimate Singapore Guide for 2026

- When to Sell Your Car in Singapore: The Strategic 2026 Guide to Maximizing Returns

- Car Dealership Financing vs Bank Loan in Singapore: The 2026 Comparison Guide