How to Calculate Car Loan Monthly Payment in Singapore: A 2026 Guide

Last week, a buyer named Sarah sat in our showroom with a detailed spreadsheet, trying to determine if a S$145,000 sedan truly fit her S$5,500 monthly income. Like many Singaporeans, she felt a wave of anxiety over how a 2.48% interest rate translates into a real-world monthly bill once you include the latest COE premiums. It's frustrating when you can't tell if a dealer's quote is a fair deal or if there's a hidden cost you've missed. You likely agree that car financing math often feels like a black box, especially when you're balancing your lifestyle against the 60% Total Debt Servicing Ratio (TDSR) limit.

We're here to replace that confusion with professional clarity. This guide teaches you exactly how to calculate car loan monthly payment using the precise formulas local banks use, giving you the tools to verify any quote with absolute confidence. We'll break down the difference between fixed and reducing interest rates, explain how 2026 COE prices affect your loan principal, and show you how to secure budget certainty before you visit a dealership.

Key Takeaways

- Understand how MAS LTV limits and your vehicle's OMV dictate your maximum borrowing capacity and required downpayment in S$.

- Learn the exact formula for how to calculate car loan monthly payment to ensure your next vehicle fits perfectly within your monthly budget.

- Compare the long-term financial impact of 5-year versus 7-year loan tenures to find the optimal "sweet spot" for your ownership cycle.

- Evaluate your loan eligibility by navigating the 55% TDSR threshold and understanding how existing debts influence your borrowing power.

- Discover how professional assistance with valuation and insurance can streamline your financing process for a seamless car-buying experience.

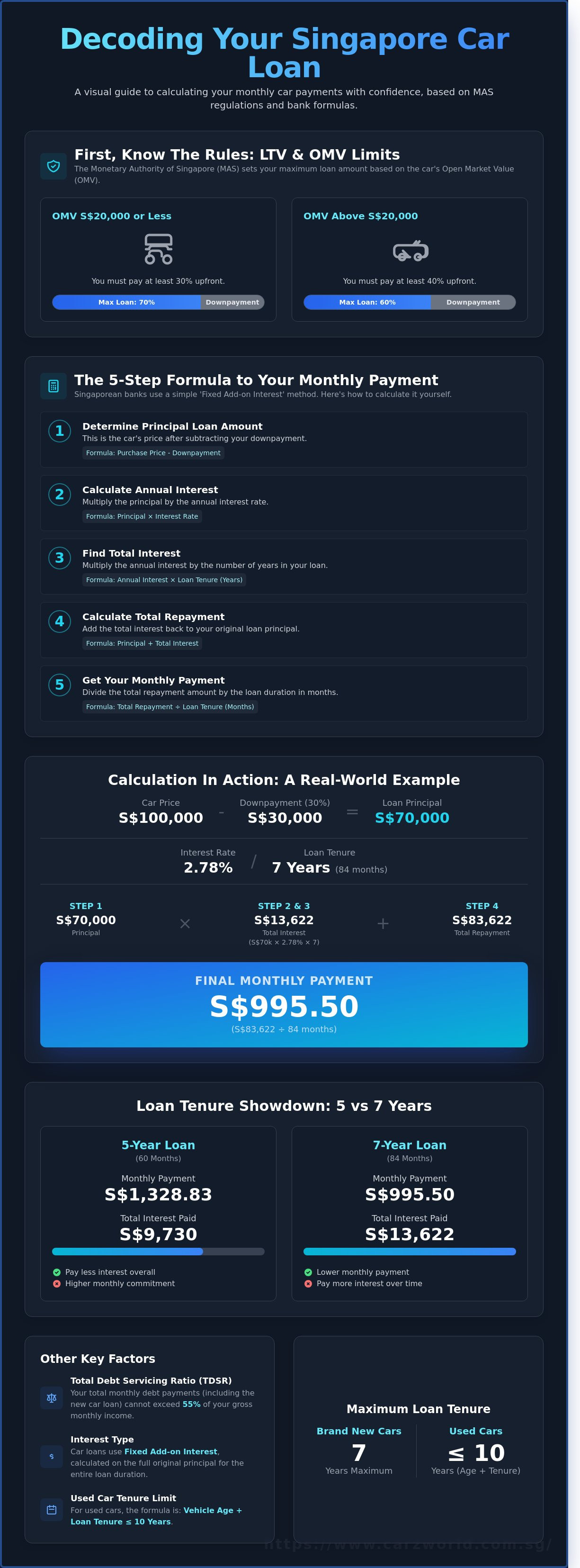

Understanding the Basics: Singapore's Car Loan Rules (LTV & OMV)

Before you learn how to calculate car loan monthly payment, you must understand the regulatory framework set by the Monetary Authority of Singapore (MAS). These rules dictate exactly how much you can borrow. Your loan eligibility isn't just based on your monthly income; it's tied directly to the car's value and the prevailing Certificate of Entitlement (COE) prices.

The actual loan amount is calculated on the net price of the vehicle. This total price includes the base cost, GST, and the COE. You don't borrow the full sticker price. Instead, you must pay a mandatory downpayment upfront. The remaining balance, after this downpayment is subtracted, becomes your principal loan amount. Since COE prices for Category A and B often exceed S$80,000 or S$100,000, this component significantly inflates the total price and, consequently, your monthly commitment.

The OMV Thresholds for 2026

The Open Market Value (OMV) is the price of the car before taxes, dealer margins, and COE. It represents the "true" value of the vehicle as it arrives in Singapore. For 2026, MAS uses the OMV to determine your Loan-to-Value (LTV) limit:

- OMV S$20,000 or less: You can borrow a maximum of 70% of the purchase price. This means you need a 30% downpayment.

- OMV above S$20,000: Your maximum loan is capped at 60% of the purchase price. You'll need to prepare a 40% downpayment.

Understanding these tiers is the first step in knowing how to calculate car loan monthly payment. A car with an OMV of S$20,001 requires a much larger cash outlay than one at S$19,999 due to that 10% difference in the required downpayment.

Maximum Loan Tenure in Singapore

The standard maximum tenure for a car loan in Singapore is 7 years, or 84 months. While a longer tenure makes each installment smaller, it increases the total interest you'll pay over the life of the loan. If you're exploring used cars, the rules are more restrictive. Most banks require that the age of the vehicle plus the loan tenure does not exceed 10 years. For example, if you purchase a car that's already 6 years old, your maximum loan term will likely be capped at 4 years. Pre-owned vehicles also involve different valuation rules that can affect the final loan amount offered by the bank.

The Step-by-Step Formula: How to Calculate Your Monthly Payment

Understanding the math behind your financing helps you stay in control of your budget. In Singapore, most automotive lenders use the fixed-rate add-on method. This makes it easier to predict your expenses because your monthly commitment remains constant throughout the loan term. When you learn how to calculate car loan monthly payment amounts manually, you gain the clarity needed to compare different bank offers effectively.

To find your monthly figure, follow these five logical steps:

- Step 1: Determine your Principal Loan Amount. This is the total purchase price of the vehicle minus your cash downpayment. For example, if a car costs S$100,000 and you pay S$30,000 upfront, your principal is S$70,000.

- Step 2: Calculate Annual Interest. Multiply your principal by the annual interest rate offered by the bank.

- Step 3: Find Total Interest. Multiply the annual interest by the number of years in your loan tenure.

- Step 4: Calculate Total Repayment. Add the total interest from Step 3 back to your original principal amount.

- Step 5: Final Division. Divide the total repayment amount by the total number of months in your loan term to get your monthly installment.

The 'Monthly Car Payment Formula' Explained

The standard formula used by Singaporean financial institutions is: Monthly Payment = [Principal + (Principal x Interest Rate x Years)] / Total Months. It's vital to distinguish between 'Fixed Add-on Interest' and 'Reducing Balance Interest.' While home loans use a reducing balance where interest drops as you pay down the debt, car loans typically use fixed add-on rates. This means your interest is calculated on the full original principal for the entire duration; it doesn't decrease even as your outstanding balance shrinks.

A Practical Calculation Example

Let's apply this to a real-world scenario. If you're looking at brand new cars priced at S$100,000, you'll likely face a 30% downpayment requirement of S$30,000. This leaves you with a loan principal of S$70,000. With a typical 2026 market interest rate of 2.78% over a 7-year tenure (84 months), the breakdown looks like this:

- Annual Interest: S$70,000 x 0.0278 = S$1,946

- Total Interest over 7 years: S$1,946 x 7 = S$13,622

- Total Repayment Amount: S$70,000 + S$13,622 = S$83,622

- Monthly Installment: S$83,622 / 84 months = S$995.50

This transparent approach ensures you won't face surprises when signing your hire purchase agreement. Knowing how to calculate car loan monthly payment figures allows you to adjust your downpayment or loan tenure until the numbers fit your lifestyle perfectly.

Analyzing the Impact of Loan Tenure: 5 Years vs. 7 Years

Choosing between a five-year and a seven-year tenure is a strategic decision for any Singaporean car buyer. While a longer tenure makes a premium vehicle feel more affordable today, it adds to the total cost of ownership over time. Understanding how to calculate car loan monthly payment totals involves more than just looking at the sticker price; it requires balancing your monthly budget against long-term interest costs.

Monthly Cashflow vs. Total Interest Cost

Let's look at a concrete example using an S$80,000 loan principal at a standard flat interest rate of 2.78%. If you opt for a 5-year tenure, your monthly installment is approximately S$1,518. Over the full 60 months, you'll pay S$11,120 in total interest. If you stretch that same loan to 7 years, your monthly payment drops to about S$1,137, giving you S$381 in extra disposable income every month.

However, that 24-month extension isn't free. The total interest on the 7-year loan jumps to S$15,568. That's an extra S$4,448 in interest "wastage." You're essentially paying a premium for the convenience of lower monthly bills. For most Singaporeans, the 5-year mark is the "sweet spot" because it aligns with the typical car ownership cycle before maintenance costs rise.

Early Settlement and the Rule of 78

The 10-year COE cycle in Singapore heavily influences loan decisions. Many owners choose to upgrade their vehicle around the 5th or 6th year. If you've taken a 7-year loan and decide on selling your car at year five, you'll encounter the Rule of 78. This is a mathematical formula banks use to front-load interest payments.

In the first two years of your loan, your installments go mostly toward interest rather than the principal amount. When you settle the loan early, the bank doesn't simply waive the remaining interest. They apply a penalty and a rebate formula that often leaves you with a higher outstanding balance than you'd expect.

- Principal Debt: A 7-year loan clears the principal slower, which could lead to "negative equity" where you owe the bank more than the car's market value.

- COE Expiry: Taking a 7-year loan leaves you with only three years of debt-free driving before the 10-year COE expires.

- Rebate Reality: Under the Rule of 78, you'll likely receive less than 50% of the remaining interest as a rebate if you settle halfway through the term.

When you learn how to calculate car loan monthly payment schedules, always account for these hidden settlement costs. It's often better to choose a shorter tenure that fits your budget to ensure you're building actual equity in your vehicle faster.

Beyond the Formula: TDSR and Loan Eligibility in 2026

Knowing how to calculate car loan monthly payment is only half the battle. In Singapore, your eligibility depends heavily on the Total Debt Servicing Ratio (TDSR), which is currently capped at 55%. This rule ensures you don't overextend your finances. Every debt counts. Your housing loan, credit card balances, and even that personal loan for your renovation factor into the math. If your total debt obligations exceed 55% of your gross monthly income, banks will reject your application regardless of your savings.

Lenders also scrutinize your Credit Bureau Singapore (CBS) report. A credit score of AA or BB makes the process seamless. However, if you've missed payments recently, your score might drop to HH, which signals high risk. Major banks follow these MAS regulations strictly. If you find your TDSR is too high, in-house finance options often provide more flexible criteria, though they might come with slightly different interest structures. Our team at Carz World can help you compare these options to find a fit that suits your financial profile.

Calculating Your TDSR Limit

To find your limit, sum up all monthly debt repayments. For example, if you earn S$6,000 a month, your total debt cap is S$3,300. If your home loan is S$2,000 and credit card installments are S$500, you only have S$800 left for a car loan. If the car loan pushes you to S$850, you've crossed the 55% threshold. You can improve your chances by clearing small debts. Paying off a S$2,000 personal loan entirely can suddenly open up the "debt room" you need for your dream car.

Hidden Costs to Include in Your Budget

Your monthly installment is just one part of the equation. We often tell our customers that the monthly payment should only represent about 70% of your total monthly car budget. You must account for recurring costs that don't show up in a standard loan calculator:

- Road Tax: This varies by engine capacity and can cost hundreds of dollars annually.

- Insurance Premiums: Comprehensive coverage is mandatory for cars under a loan.

- Maintenance: Set aside at least S$100 to S$150 monthly for servicing and wear-and-tear parts.

- COE Fluctuations: If you are eyeing brand new cars, keep in mind that COE prices can shift by S$5,000 to S$10,000 between bidding cycles.

Planning for these extras ensures you don't just own the car, but can actually afford to drive it. If you're unsure about your current eligibility, Talk to our consultants for a personalized assessment.

Navigating Your Car Financing with Carz World

Choosing a vehicle is exciting, but the financial paperwork often feels overwhelming. At Carz World, we act as a direct bridge between you and Singapore's major financial institutions. This partnership ensures you get competitive interest rates without the stress of shopping around. We provide a one-stop service that handles your valuation, loan processing, and insurance in a single location. This efficiency saves you time and prevents the confusion that often comes with managing multiple vendors during a purchase.

Transparency is the foundation of our business model. Many buyers find that hidden admin fees or unexpected processing charges skew their initial budget. We eliminate these surprises. When you learn how to calculate car loan monthly payment requirements, you need honest numbers to get an accurate result. Our pricing is straightforward, so the figure you calculate is the figure you actually pay. Our team focuses on being helpful and patient rather than pushy, a trait frequently highlighted in our 5-star customer reviews.

Personalized Loan Consultations

Every buyer has a unique financial profile. You can sit down with our experienced consultants, like Ryan, Carson, Adam, or Ben, to run your specific numbers. They help you understand the nuances of different packages, whether you're looking at export cars for international use or a reliable sedan for local roads. If you prefer to start from home, you can request a quote directly through our digital portal to see your options quickly. It's a professional way to see what you can afford before you commit.

Lowering Your Monthly Payment via Trade-In

The most effective way to reduce your monthly commitment is to lower the principal loan amount. Carz World offers a high-valuation trade-in service to help you achieve this. We provide two main paths for your current vehicle:

- Direct Trade-In: Receive an immediate, competitive offer to offset your new car's cost.

- Consignment Advantage: Let us sell your car on your behalf to secure a potentially higher market price for your old vehicle.

By maximizing the value of your old car, you decrease the total amount you need to borrow. This simple step makes it much easier when you determine how to calculate car loan monthly payment schedules that fit your lifestyle. Visit our showrooms at Vertex or Alexandra today for a smooth process and professional advice from a team that values your trust and long term satisfaction.

Drive Home with Confidence and Clarity

Navigating the 60% or 70% LTV limits and 2026 TDSR regulations is the first step toward owning your next vehicle. While a 7-year tenure provides lower monthly outgoings, the total interest paid is often higher than a 5-year plan. Mastering how to calculate car loan monthly payment figures ensures you stay within a sustainable budget. Carz World removes the guesswork from your financing journey. We're a direct partner with major Singapore banks including DBS, UOB, and OCBC. This allows us to provide transparent interest rates with no hidden fees. More than 100 customers have voted us 'Highly Recommended' for our professional and patient service. Our methodical approach ensures your trade-in and handover are seamless. Talk to our experts today for a personalized car loan quote. You've done the research; now let's get you behind the wheel with a plan that works for your lifestyle.

Frequently Asked Questions

What is the minimum downpayment for a car in Singapore in 2026?

The minimum downpayment for a car in Singapore in 2026 depends on the vehicle's Open Market Value (OMV). For cars with an OMV of S$20,000 or less, you're required to pay at least 30% of the purchase price upfront. If the OMV exceeds S$20,000, the minimum downpayment increases to 40% as per Monetary Authority of Singapore (MAS) regulations. These rules ensure buyers maintain sustainable debt levels while purchasing high quality vehicles.

Can I use a car loan calculator for both new and used cars?

Yes, you can use a calculator for both new and pre-owned vehicles to estimate your budget. While the tool helps you understand how to calculate car loan monthly payment figures, keep in mind that interest rates for used cars are usually 1% to 1.5% higher than for brand new models. Our consultants provide a transparent breakdown for both categories to make your buying process a seamless and pleasant one.

Is it better to take a bank loan or in-house dealer financing?

Choosing between a bank and in-house financing depends on your priority for interest rates versus approval speed. Banks typically offer lower rates, averaging around 2.78% per year, but they have very strict credit requirements. In-house dealer financing offers more flexibility and faster processing, which is helpful if you want a smooth handover. We've found that customers appreciate having both options to ensure a professional and honest transaction.

How does the 'Fixed Add-on' interest rate differ from a home loan rate?

A 'Fixed Add-on' rate calculates interest based on the original loan amount for the entire duration, whereas home loans use a reducing balance method. This means you're paying interest on the full principal even as you pay it down over time. It's a crucial factor when you learn how to calculate car loan monthly payment amounts because a 2.78% flat rate actually equals an Effective Interest Rate (EIR) of about 5.2%.

What documents do I need to prepare for a car loan application?

You need to provide your NRIC or passport, your latest 3 months of payslips, and your CPF Contribution History for the last 12 months. Self-employed buyers must include their latest 2 years of Income Tax Notice of Assessment (NOA). Having these documents ready allows our staff to process your application quickly. It's a methodical approach that helps us maintain our reputation for excellent service and efficiency.

Can foreigners in Singapore apply for a car loan?

Foreigners can apply for a car loan if they hold a valid Employment Pass with at least 6 months of validity remaining at the time of application. Most Singaporean banks require a local guarantor if the applicant has lived in the country for less than 12 months or if the loan amount is particularly high. We've helped many expatriates navigate these requirements to secure well maintained vehicles through a dependable and clear process.

What happens to my car loan if I sell my car before the tenure ends?

When you sell your car before the loan ends, you must pay off the remaining balance plus an early settlement penalty, which is usually 1% of the original loan. You'll receive an interest rebate based on the Rule of 78, though this amount is often smaller than expected. Our team makes this trade-in process simple by handling the bank settlements directly, ensuring a smooth transition to your next vehicle.

Does the COE price affect my monthly loan instalment?

The COE price significantly affects your monthly instalment because it's included in the total purchase price of the car. Since the COE can represent 50% or more of the total cost in the current market, a higher bidding price increases your total loan principal. This results in a larger monthly commitment even if the interest rate stays at 2.78%. We always provide a detailed quote so you see exactly how the COE impacts your costs.

In Same Category

- How to Get a Fair Trade-In Offer for Your Car in Singapore: 2026 Guide

- Selling a Car with an Outstanding Loan in Singapore: The 2026 Complete Guide

- Car Consignment vs Direct Sale in Singapore: The 2026 Seller’s Guide

- How to Avoid Overpaying for a Used Car in Singapore (2026 Guide)

- 15 Practical Saving Tips for Car Buyers in Singapore (2026 Edition)