How Much Savings Do You Need Before Buying a Car in Singapore? (2026 Guide)

What if the biggest risk of owning a car in 2026 isn't the $100,000 COE price tag, but the hidden restoration buffer you forgot to save? It's a common trap. Many drivers focus only on the monthly instalment and find themselves car-poor shortly after signing the papers. Determining exactly how much savings before buying a car in singapore is necessary requires looking far beyond the sticker price. With GST at 9% and MAS rules requiring a 40% downpayment for any car with an OMV over $20,000, your upfront liquidity must be calculated with professional precision.

We understand that you want the freedom of the road without the constant stress of a thinning bank account. This guide provides the exact math you need to safely commit to a vehicle, whether it's a brand new model or a high quality pre-owned car. You'll discover our Triple-Layer savings framework, covering everything from tiered ARF calculations to the specific maintenance buffers needed for older vehicles under the new 2026 PARF rebate rules. By the end, you'll have a clear dollar-value target for your savings account and the confidence to make a move.

Key Takeaways

- Learn the specific downpayment math based on OMV tiers to avoid unexpected cash shortfalls during the registration process.

- Discover exactly how much savings before buying a car in singapore you should reserve for the Triple-Layer strategy, including insurance and maintenance buffers.

- Master the 30/20 financial framework to ensure your vehicle purchase fits comfortably within your monthly budget and long-term goals.

- Explore how choosing high quality pre-owned cars or parallel imports can significantly lower your initial capital requirements without sacrificing reliability.

Evaluating Your Readiness: Why Savings Matter More Than Salary

Many aspiring drivers focus solely on their monthly paycheck. While a steady income is vital for loan approval, it doesn't tell the whole story. In the local market, the entry barrier is often more daunting than the monthly running costs. You might earn $8,000 a month, but if you don't have the liquid cash for the initial 30% or 40% downpayment, your purchase won't move forward. Understanding how much savings before buying a car in singapore you actually need is the first step toward a seamless ownership experience.

To better understand the financial commitment involved in high-value purchases, watch this helpful video:

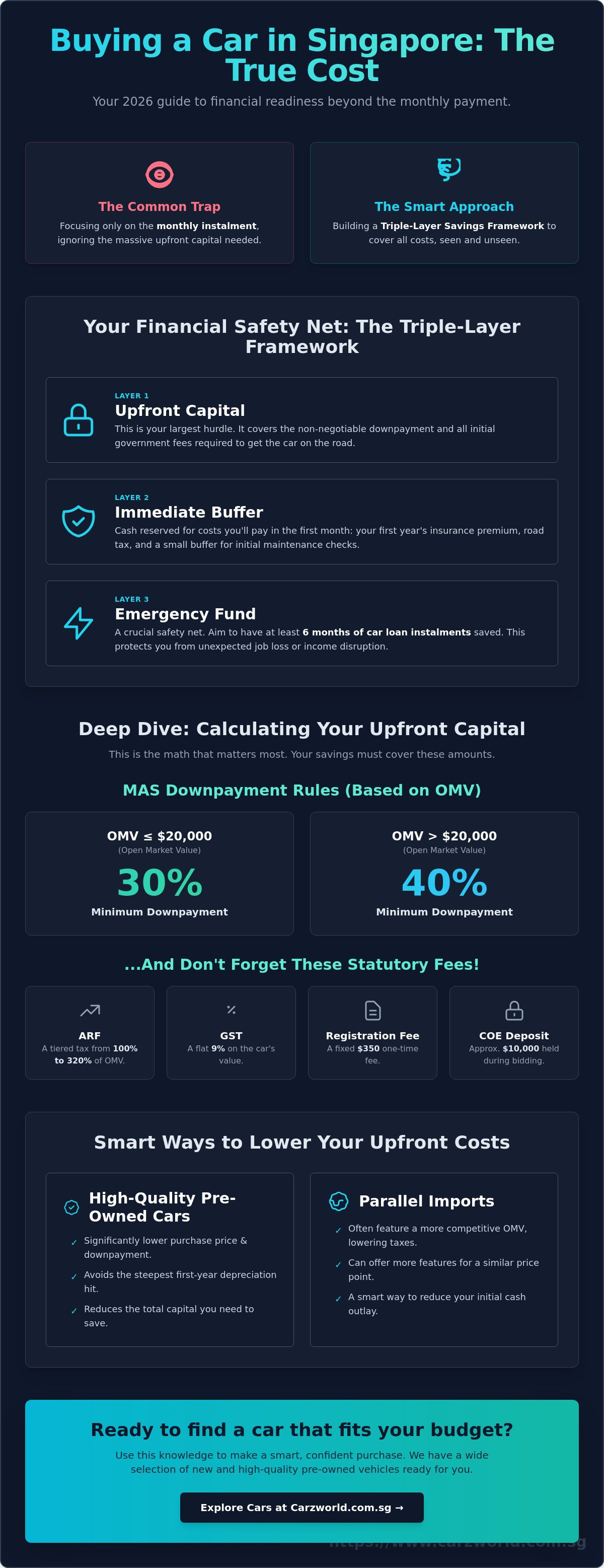

We recommend a Triple-Layer savings framework to protect your lifestyle. The first layer is your Upfront Capital, which covers the downpayment and registration. The second is the Buffer Layer, intended for immediate costs like insurance and road tax. Finally, the Emergency Layer provides six months of instalments as a safety net. This structure ensures you won't feel car-poor even if unexpected expenses arise. Having this reserve offers a psychological peace of mind that a high salary alone cannot provide.

Cash Flow vs. Liquidity: The Singapore Dilemma

The Hire Purchase Act and Total Debt Servicing Ratio (TDSR) regulations significantly impact your buying power. Banks don't just look at what you earn; they scrutinize your existing debt obligations. If your cash flow is tied up in property loans or credit card balances, your car loan eligibility shrinks. Determining how much savings before buying a car in singapore is necessary involves calculating how much liquid cash you can part with without affecting your debt ratios. There's a massive difference between affording the car and affording the lifestyle. Without sufficient liquidity, you may find your monthly disposable income stretched too thin.

The 2026 Car Market Context

As of March 2026, Certificate of Entitlement (COE) prices remain at historic highs, often exceeding $100,000. These volatile premiums mean the minimum cash-on-hand requirement is much higher than in previous years. While some buyers wait for prices to drop, history shows that timing the market is difficult and can result in higher costs if premiums rise further. Total Liquidity is the sum of your downpayment, statutory fees, and a 15% emergency buffer. When you're ready to make a move, choosing high quality pre-owned vehicles can help manage these upfront hurdles more effectively.

Calculating the Upfront Capital: Downpayment and Statutory Fees

The first hurdle in your car ownership journey is the downpayment. In Singapore, the amount of liquid cash you need is strictly dictated by the vehicle's Open Market Value (OMV). This is why calculating how much savings before buying a car in singapore is so specific to the model you choose. If the car's OMV is $20,000 or less, you can borrow up to 70% of the purchase price, requiring a 30% downpayment. However, for most modern vehicles with an OMV exceeding $20,000, you must provide a 40% downpayment upfront.

These MAS car loan regulations are non-negotiable and designed to ensure buyers maintain a healthy financial profile. Beyond the downpayment, you must also account for the $350 Registration Fee and the Additional Registration Fee (ARF). The ARF is a tiered tax that starts at 100% of the OMV and can climb as high as 320% for luxury models. In 2026, the 9% GST is also applied to the OMV plus the Excise Duty, adding another layer to your initial cash requirement. When your dealer bids for a Certificate of Entitlement, they typically require a deposit of around $10,000, which stays locked up during the process. If you are looking for brand new cars, ensure your savings pot accounts for these temporary but necessary outflows.

The LTA Loan-to-Value (LTV) Framework

Consider Scenario A: a Japanese hatchback with an OMV of $19,000. Under the 30% rule, your downpayment might seem manageable. But when you add a $100,000 COE and the ARF, the total purchase price easily crosses $150,000. This means you need at least $45,000 in liquid cash just for the downpayment. In Scenario B, a Continental SUV with an OMV of $45,000 changes the math significantly. You now face a 40% downpayment requirement. With the higher tiered ARF, the total price could hit $250,000, pushing your savings target for the downpayment alone to $100,000. Aiming for the minimum downpayment isn't always the best strategy. If your savings allow, a larger upfront payment reduces your monthly instalments and total interest paid over the seven year loan tenure.

Statutory Fees You Must Save For

The ARF is often the most significant "hidden" cost. While you pay this upfront, it's important to understand the 2026 PARF rebate system. For a car deregistered between nine and ten years of age, the rebate is now capped at 5% of the ARF, or a maximum of $30,000. This change means you'll recover less of your initial "savings" at the end of the car's life compared to previous years. You must also factor in the 20% Excise Duty on the OMV before the 9% GST is applied. These numbers can be complex, but getting them right is essential for a smooth process. If you need a precise breakdown for a specific model, you can talk to us for a professional consultation.

The Hidden Buffers: Savings Needed for Insurance, Road Tax, and Maintenance

The purchase price is simply the price of admission. To truly understand how much savings before buying a car in singapore is required, you must look at the first six months of ownership. Many buyers overlook the "Used Car Restoration Fund," which is a critical buffer of $3,000 to $5,000 for pre-owned vehicles. This cash reserve ensures that even if you find a high quality unit, you can immediately address minor wear and tear without stressing your monthly budget. It's the difference between enjoying your new ride and worrying about every trip to the workshop.

Insurance and Road Tax: The Year 1 Outlay

Your first year of ownership comes with heavy upfront recurring costs. Most hire-purchase agreements require comprehensive insurance, which can be expensive for younger drivers or those with a low No Claims Discount (NCD). A younger driver with less than three years of experience might need a larger savings cushion to handle high-excess policies. Additionally, road tax is an annual expense based on engine capacity. For a 1.6L sedan, the annual road tax is approximately $740. We recommend creating a holistic car ownership budget that accounts for these statutory payments before you sign the agreement. This ensures you aren't caught off guard when the renewal notice arrives in your mailbox.

The Maintenance Sinking Fund

Even a well-maintained used car singapore requires a dedicated maintenance sinking fund. We suggest saving at least 10% of the car's purchase value as a dedicated repair buffer. Within the first 12 months, you'll likely face standard wear and tear items such as new tyres, a fresh battery, or braking system components. While buying from a professional dealer often means the car has undergone a thorough inspection, having this cash on hand prevents a "smooth process" from turning into a financial headache. A dedicated fund keeps your vehicle in pristine condition and preserves its long-term resale value.

Beyond mechanical needs, don't forget the liquid reserve for petrol and parking. In 2026, most drivers find that monthly variable costs range between $500 and $800. This includes season parking at your HDB or office, fuel costs, and ERP charges. When calculating how much savings before buying a car in singapore you need, ensure your bank account can absorb these daily expenses without depleting your primary emergency fund. Planning for these hidden buffers is what separates a prepared car owner from one who becomes car-poor within the first year.

Prudent Financial Frameworks: How to Know If You're Ready to Buy

Determining how much savings before buying a car in singapore is necessary goes beyond simply meeting the minimum legal requirements. You need a framework that ensures the car serves your lifestyle rather than draining your future wealth. We recommend the 30/20 Rule as a professional benchmark. This involves providing at least a 30% downpayment while ensuring your total monthly vehicle costs, including instalments, fuel, and parking, don't exceed 20% of your total household income. This buffer protects you from becoming car-poor if your other living expenses fluctuate.

Another reliable metric is the One-Year Salary Benchmark. Ideally, the total price of your car, including the COE, shouldn't exceed your annual gross pay. If you earn $120,000 a year, committing to a vehicle priced at $220,000 creates a heavy debt burden that could last for seven years. You should also stress-test your savings against the current volatility of the 2026 market. If COE prices rise by 10% before your bid is successful, you must have the liquid cash to cover the difference. A 'Walk-Away' Fund of six to twelve months of living expenses should remain untouched in your bank account after you've paid for the car.

Step-by-Step Financial Stress Test

Start by subtracting your total upfront cash, including the downpayment and all statutory fees, from your current savings. A 'ready' buyer has at least $10,000 in liquid cash remaining after all car-related downpayments. Next, calculate your new monthly surplus after accounting for the car loan and variable costs like petrol. If your remaining disposable income feels tight, it's a sign that you need to build a larger capital base. When you calculate how much savings before buying a car in singapore you truly need, this surplus is your most important safety net.

The Opportunity Cost of Car Savings

Every dollar spent on a vehicle is capital that isn't earning interest in a diversified portfolio. If the $100,000 used for a downpayment could earn 5% annually elsewhere, the true cost of ownership includes that lost growth. Sometimes the convenience of a car outweighs these costs, particularly for families or those with long commutes. If you're still building your capital, car rental serves as an excellent bridge. It provides immediate mobility while allowing your savings to grow until you hit your target. When you've reached that financial milestone, you can talk to us to explore our latest inventory and find a vehicle that fits your budget perfectly.

Optimising Your Budget: How Used Cars and Parallel Imports Reduce Capital Requirements

If you find that the upfront capital for a showroom-fresh model is too high, there are strategic ways to lower the barrier. Choosing a five year old pre-owned car is often the 'sweet spot' for savings-conscious buyers. At this stage, the steep initial depreciation has already occurred, yet the vehicle typically retains five years of COE life. Because the total purchase price is lower, your 30% or 40% downpayment hurdle becomes significantly easier to clear. When calculating how much savings before buying a car in singapore you need, these pre-owned options can reduce your required cash-on-hand by tens of thousands of dollars.

For those who prefer brand new cars, Parallel Imports (PI) offer a compelling alternative. PI models often come with more competitive price tags than those from authorized distributors, directly reducing the 9% GST and ARF components of your upfront costs. This allows you to own a new vehicle while keeping a larger portion of your emergency reserve intact. You might also consider the consignment advantage. Buying directly from an owner through a professional dealer eliminates heavy markups. Our methodical approach ensures that while you save on costs, the car remains in pristine condition.

The Math of Pre-Owned Savings

The lower purchase price of a used car doesn't just mean a smaller loan; it drastically shrinks the initial savings requirement. By paying only for the 'COE Remaining,' you avoid the massive upfront premium of a ten year certificate. Our 'not pushy' consultants focus on finding a car that fits your actual savings rather than pushing for your maximum loan eligibility. This honest approach ensures your car ownership journey remains a pleasant one. When you choose a high quality unit that has been well maintained, you can also reduce the size of the maintenance buffer discussed in previous sections.

Next Steps: From Saving to Driving

The final step in your journey is to turn your current assets into liquid capital. Getting a professional valuation for your current ride can significantly boost your downpayment, lowering the amount of additional savings you need to deploy. We provide a smooth process for trade-ins, ensuring you get a fair price to offset your next purchase. You can also request a no-obligation quote to see the real numbers behind the models you're interested in.

Ready to see what your savings can buy? Discover our high-quality pre-owned collection today. Whether you're looking for a reliable daily driver or a premium SUV, we're here to help you navigate the 2026 market with confidence. Our team ensures every handover is a seamless experience, letting you enjoy the road without financial worry.

Start Your Ownership Journey with Confidence

Success in the 2026 car market requires more than just a high salary; it demands a disciplined approach to liquidity. By applying the Triple-Layer savings framework and the 30/20 rule, you ensure that your vehicle remains an asset to your lifestyle rather than a burden. Knowing exactly how much savings before buying a car in singapore you need allows you to navigate OMV tiers and tiered ARF taxes without surprises. Whether you choose a certified pre-owned unit or a brand new parallel import, having a six month instalment reserve provides the peace of mind every driver deserves.

At Carz World, we believe in transparent pricing with no hidden admin fees on our used car handovers. Our expert consultants have earned over 1,000+ 5-star reviews by providing patient, not-pushy service that prioritizes your financial health. We're here to help you find a high quality vehicle that fits your budget perfectly. Talk to our expert consultants for a seamless car buying experience today. You've done the math; now it's time to enjoy the road ahead.

Frequently Asked Questions

What is the absolute minimum cash downpayment for a car in Singapore?

The minimum cash downpayment is 30% of the purchase price for vehicles with an Open Market Value (OMV) of $20,000 or less. If the OMV exceeds $20,000, MAS regulations require a 40% downpayment. This amount must be paid in liquid cash or through a trade-in value, as it cannot be covered by the car loan itself. Ensuring you have this capital ready is the first step in the ownership process.

Can I use my CPF savings to buy a car?

No, you cannot use your CPF savings for any part of a car purchase in Singapore. CPF funds are strictly reserved for retirement, housing, and healthcare needs. Every cost associated with vehicle ownership, from the initial downpayment to road tax and insurance, must be paid using your personal cash savings or monthly disposable income. This is why building a dedicated car fund is essential before you begin shopping.

How much should I set aside for car insurance in my first year?

You should budget between $1,500 and $3,500 for your first year of comprehensive insurance. The exact amount depends on your age, driving experience, and No Claims Discount (NCD) status. Younger drivers under 27 years old often face higher premiums and excesses. Since comprehensive coverage is a requirement for all hire-purchase loans, having this liquid cash available is a vital part of your initial savings plan.

Is it better to save for a larger downpayment or take a maximum loan?

Saving for a larger downpayment is usually the more prudent financial move. While a maximum loan preserves your immediate liquidity, it increases the total interest you pay over the seven year tenure. A larger upfront payment reduces your monthly debt obligations and provides better protection against future interest rate hikes. This strategy ensures your monthly cash flow remains healthy and helps you avoid becoming car-poor over the long term.

How much does road tax cost for a typical 1.6L car?

The annual road tax for a typical 1.6L petrol engine is approximately $740 as of 2026. This is a recurring statutory fee that must be paid every six or twelve months. Owners of smaller 1.0L turbocharged models enjoy a lower rate of approximately $600 per year. When calculating how much savings before buying a car in singapore you need, always include these recurring annual fees in your first year budget.

What happens if I don't have enough savings for the 30% downpayment?

If you don't meet the minimum 30% downpayment threshold, you won't be able to secure a car loan from any regulated financial institution. In this situation, the best course of action is to continue saving or explore car rental options. Rental services allow you to stay mobile without a massive capital outlay. This gives you the time needed to build your savings until you can comfortably afford the upfront costs of ownership.

Should I save more for a new car or a used car?

New cars require a much larger savings pot because of higher purchase prices and tiered ARF taxes. Used cars have lower entry barriers but require a larger maintenance buffer for wear and tear items. Determining how much savings before buying a car in singapore is necessary depends on your priorities. If you want lower monthly costs, save more for a new car; for lower upfront capital, a high quality pre-owned unit is better.

How much of an 'emergency buffer' is recommended for car-related repairs?

We recommend a dedicated maintenance buffer of $3,000 to $5,000 for any pre-owned vehicle purchase. This fund covers immediate needs like new tyres, battery replacements, or brake servicing within the first year. For general financial safety, you should also keep at least six months of car instalments in a separate emergency account. This ensures that a sudden workshop visit or a change in employment doesn't compromise your ability to keep your car.

In Same Category

- How to Prepare Your Car for Sale in Singapore: The Ultimate 2026 Checklist

- When to Sell Your Car in Singapore: The Strategic 2026 Guide to Maximizing Returns

- Car Dealership Financing vs Bank Loan in Singapore: The 2026 Comparison Guide

- Used Car Warranty in Singapore: The Ultimate Guide to Protection in 2026

- Used Car Service History Check Singapore: The 2026 Ultimate Buyer’s Guide