Car Loan for New Permanent Residents in Singapore: The 2026 Ultimate Guide

What if your newly minted blue NRIC was the secret to slashing your monthly transport expenses? For many, securing a car loan for new permanent resident sg status is the final piece of the puzzle in settling into local life in 2026. You've likely felt the frustration of high expat rental costs or the anxiety that a short residency duration might lead to a credit rejection. At Carz World Pte Ltd, we believe your residency status should be a gateway to better opportunities, not a hurdle to clear.

We promise to help you master the complexities of Singapore's 2026 financing landscape so you can secure the best possible rates for your dream vehicle. This guide provides a clear path through the confusion of loan caps and total cost of ownership. You'll learn exactly how to navigate the application process and find a partner who handles the heavy paperwork for you. Let's explore how you can turn your PR status into a financial advantage on the road.

Key Takeaways

- Understand how the car's Open Market Value (OMV) dictates your mandatory 30% or 40% down payment under current MAS regulations.

- Organize your essential documents, including your blue NRIC and CPF history, to expedite your car loan for new permanent resident sg application.

- Compare the low interest rates of traditional bank loans against the higher flexibility and "one-stop" convenience of in-house financing.

- Take advantage of the 2026 market by factoring in the $30,000 PARF rebate cap when selecting your next vehicle model.

- Partner with Carz World Pte Ltd to ensure a seamless handover process where all LTA paperwork is managed by experienced professionals.

Navigating Car Ownership as a New Singapore Permanent Resident

Transitioning from an Employment Pass to Permanent Residency is a major lifestyle milestone. For many, this shift moves the focus from temporary car rentals to the security of long term ownership. While expats often rely on monthly leases, becoming a PR allows you to build equity in a vehicle. It's about planting roots in Singapore. You're no longer just a visitor; you're a resident with a long term stake in the country's future. Carz World Pte Ltd understands this transition and aims to make your first local car purchase as smooth as your residency application.

2026 is a unique time for this transition. The government recently capped the PARF rebate at $30,000 as of February 20, 2026. While this changes the math for high end models, it makes the pre-owned market and efficient new cars even more attractive. Securing a car loan for new permanent resident sg applicants is now about strategic planning rather than just high income. The Monetary Authority of Singapore (MAS) sets the ground rules, but your PR status is the key that opens doors to better financing terms. We see many clients who are surprised by how much their borrowing power increases once that blue NRIC is in hand.

To better understand how interest affects your long-term commitment, watch this helpful video:

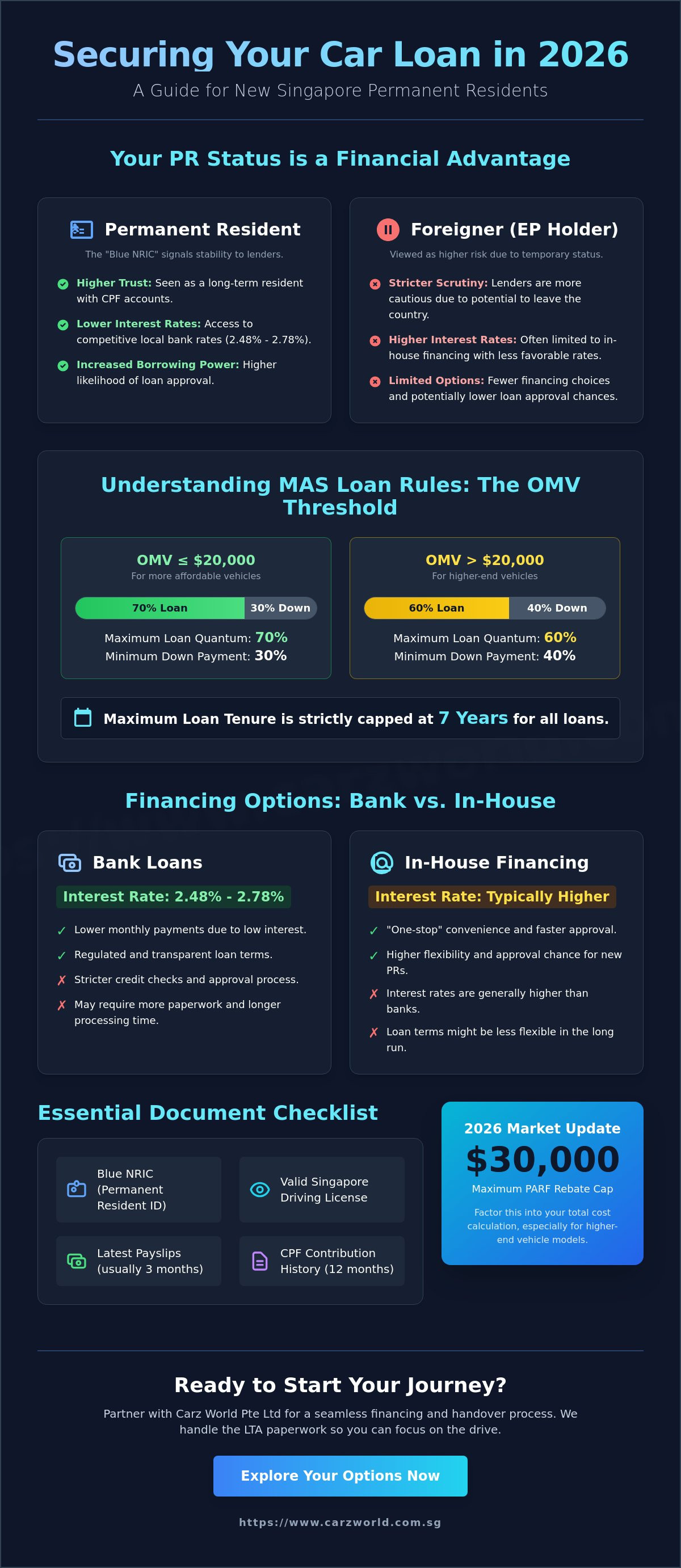

PR vs. Foreigner: The Financing Advantage

Financial institutions view PR status as a sign of stability. Unlike EP holders who might leave the country on short notice, PRs have CPF accounts and long-term residency intent. Lenders show increased trust toward residents. Banks are far more likely to approve a car loan for new permanent resident sg residents compared to those on work passes. You gain access to local bank interest rates, which currently sit between 2.48% and 2.78% for brand new vehicles. Foreigners often face stricter scrutiny or are limited to in-house financing with higher rates. At Carz World Pte Ltd, we've helped hundreds of new PRs leverage this advantage to secure lower monthly payments.

The Total Cost of Ownership in 2026

You can't just look at the sticker price. The Certificate of Entitlement (COE) remains the largest cost factor. In April 2026, Category A prices reached $123,010. Your borrowing limit depends heavily on the Open Market Value (OMV). If the OMV is $20,000 or less, you can borrow up to 70%. If it's higher, the cap drops to 60%. Explore our selection of high quality pre-owned cars to see how these OMV rules apply to different models. Beyond the loan, you must factor in the Additional Registration Fee (ARF) and the new $30,000 PARF rebate cap when calculating your total investment. Understanding these numbers is essential before signing any agreement.

Understanding MAS Loan Rules: OMV, Quantum, and Tenure for PRs

Securing a car loan for new permanent resident sg applicants requires a firm grasp of the local regulatory framework. While your PR status grants you better credibility with lenders, the Monetary Authority of Singapore (MAS) maintains strict boundaries on how much you can borrow. These MAS car loan regulations apply to all residents, but new PRs must be especially careful with how these limits interact with their other financial commitments. The rules focus on three main pillars: the value of the car, the length of the loan, and your existing debt.

The maximum loan tenure in Singapore is strictly capped at 7 years. You won't find a bank that offers a longer term for a standard vehicle purchase. This hard limit means your monthly instalments will be higher than in markets where 10-year loans are common. For a new PR, this makes the initial down payment and the car's purchase price even more critical to your monthly budget.

The OMV Threshold Breakdown

Open Market Value (OMV) is the price paid to the manufacturer for the vehicle before any taxes, duties, or surcharges are added. This figure is the baseline for your loan quantum. The "60/70 Rule" dictates your down payment based on this number:

- OMV ≤ $20,000: You can secure a 70% loan, requiring a 30% down payment.

- OMV > $20,000: You are limited to a 60% loan, meaning you must pay 40% upfront.

If you're considering a used vehicle, the "Adjusted OMV" comes into play. Lenders prorate the original OMV based on the car's age to determine the current LTV (Loan-to-Value) limit. It's a technical calculation that can catch buyers off guard, so it's wise to browse high quality pre-owned cars where the financing limits are clearly explained by the dealer.

TDSR and Your Borrowing Power

The Total Debt Servicing Ratio (TDSR) is a 55% limit on your total monthly debt obligations against your gross monthly income. This includes your car loan, HDB or private property mortgages, and even credit card balances. For a new PR, an existing home loan can significantly reduce the amount you can borrow for a vehicle. Lenders will also "haircut" variable income like commissions or bonuses by 30% when assessing your repayment ability. It's often helpful to settle outstanding credit card debts before submitting your car loan for new permanent resident sg application to maximize your eligible loan quantum.

Bank Loans vs. In-House Dealer Financing: Which Suits a New PR?

Choosing your lender is just as important as choosing your vehicle. In Singapore, you generally have two paths: traditional banks or in-house dealer financing. For a car loan for new permanent resident sg residents, the decision usually hinges on local credit history. Banks offer the most competitive rates, but they require a robust credit profile that many new PRs haven't built yet. Dealerships provide a more flexible alternative, acting as a bridge for those who are financially stable but "new" to the local system.

As of May 2026, the interest rate landscape is tiered. Bank loans for new cars typically range from 2.48% to 2.78% per annum. If you are looking at a pre-owned vehicle, expect rates between 2.98% and 3.08%. In-house financing often starts at 4.28%. While the rate is higher, the approval criteria are significantly more relaxed, making it a viable option for those who don't meet the strict "thin file" requirements of major banks.

When to Choose a Bank Loan

A bank loan is the ideal choice if you have lived and worked in Singapore for at least 24 months. Lenders look for stability. They want to see consistent CPF contributions and a clean credit score from the Credit Bureau Singapore (CBS). You will need to meet the standard car loan eligibility requirements, including a minimum income of $2,000 per month. Most bank contracts include early settlement penalties, often around 1% of the unpaid principal. If you plan to clear your debt early, factor this into your total cost.

The Benefits of In-House Dealer Financing

In-house financing offers speed and convenience that banks can't match. For a new PR, the "one-stop" nature of this service is a major relief. We handle the complex paperwork, insurance applications, and road tax renewals in a single process. This is particularly beneficial if you have recently started a new job or have a variable income from commissions. We focus on your current ability to pay rather than just your historical credit data. Browsing used car collections at a professional dealership allows you to see inventory that is already vetted for these flexible financing schemes.

Essential Documentation Checklist for Your PR Car Loan Application

Preparation is the key to a seamless and pleasant car buying experience. While the previous sections of this guide explained the rules and financing paths, your success ultimately depends on the accuracy of your paperwork. Lenders in Singapore are methodical and detail oriented. A single missing page from your tax statement can result in an immediate rejection or a significant delay in your approval. When applying for a car loan for new permanent resident sg residents, you must prove that your financial footprint is stable and verifiable.

Most applications now happen digitally through Singpass, but you still need to understand exactly what the bank or dealer is looking for. They don't just want to see that you have money; they want to see where it comes from and how consistently it arrives. For new PRs, this usually means showing a clear link between your previous expat status and your current residency through your contribution history.

The Core Document Pack

Every applicant must provide a standard set of identity and income proofs. Ensure your copies are clear and all edges of the documents are visible in your scans. The core pack includes:

- Front and back copy of your blue NRIC: This is your primary proof of residency status.

- Last 6 months of CPF contribution history: You should download this as a digital extract directly from the CPF portal. It provides the most reliable evidence of your employment and salary.

- Latest 2 years of IRAS Notice of Assessment (NOA): This confirms your annual income and tax compliance. Even if you were on an EP for part of this period, these records are essential.

- Letter of Appointment: If you have been with your current employer for less than six months, a signed letter of appointment helps prove your job stability and monthly remuneration.

Additional Requirements for Business Owners and Self-Employed PRs

If you run your own company, the credit assessment is more thorough. Lenders need to see the health of your business alongside your personal finances. You will need to provide an ACRA business profile that is dated within the last 3 months. This ensures the information about your company directors and shareholding is current. You must also submit your corporate bank statements for the last 6 months. These statements show the cash flow and liquidity of your operations. Finally, your personal income tax statements for the last 2 years will be used to verify your actual take home pay from the business.

Organizing these documents early allows you to move quickly when the right vehicle becomes available. If you have your paperwork ready and want to begin the process, talk to our experienced consultants for a professional review of your eligibility.

Why New PRs Choose Carz World for Seamless Financing and Handover

Finding a vehicle that fits your new life in Singapore is a major milestone. However, the technical paperwork involved in a car loan for new permanent resident sg applicants can often feel overwhelming. Carz World acts as your experienced partner, bridging the gap between your financial stability and the bank's strict requirements. We have a proven track record of assisting new PRs with complex loan cases, especially for those who have limited local credit history but strong professional backgrounds.

Our approach is fundamentally customer centric. We don't believe in aggressive sales tactics or urgent pressure. Instead, our consultants provide a "not pushy" environment where your long term financial health is the priority. We specialize in parallel imports and high quality pre-owned vehicles that are well maintained and ready for the road. Once your financing is secured, we manage the entire handover process. This includes handling the LTA transfer and all necessary registration paperwork so you don't have to spend your time in queues.

A Trusted Partner in Your PR Journey

Experience matters when you deal with Singapore's technical automotive regulations. Our consultants, including highly recommended team members like Carson and Adam, provide personalized service tailored to your specific residency timeline. We believe in total transparency. You won't find hidden "admin fees" or surprise charges during our loan processing. If you're looking to upgrade from a vehicle you already own, selling your current car through our platform is a smooth process that can help offset the down payment for your next vehicle.

Next Steps: Get Your Pre-Approval Today

We encourage all new residents to seek a loan quote before they even step into a showroom. Knowing your exact borrowing power saves time and prevents disappointment during the car search. Our team provides a clear picture of your eligible interest rates and monthly instalments based on the latest 2026 market data. You can visit us at our showrooms in Vertex or Alexandra Central to see our latest inventory in person. If you're ready to start your application, request a personalized car loan quote from the Carz World team today and experience a truly seamless transition to car ownership.

Start Your Singapore Road Journey with Confidence

Transitioning to permanent residency opens significant doors for vehicle ownership in Singapore. You now have the leverage to move beyond temporary rentals and secure a long term asset. By mastering the MAS 60/70 rule and preparing your digital document pack early, you've already cleared the biggest hurdles. Whether you choose a competitive bank rate or a flexible in-house option, your status is your strongest asset in the 2026 market.

Securing a car loan for new permanent resident sg applicants doesn't have to be a source of anxiety. At Carz World, we take pride in our 4.9-star rated service, specifically designed to help expats and new residents navigate these complexities. As a direct parallel importer of the latest models, we offer a wide range of options paired with transparent in-house financing. We handle the technical LTA transfers and paperwork so you can focus on the road ahead.

Drive home your dream car with a PR-friendly loan from Carz World. We look forward to helping you settle into your new life with a vehicle that matches your ambitions.

Frequently Asked Questions

Can a new PR get a 100% car loan in Singapore?

No, you cannot get a 100% car loan in Singapore due to strict MAS regulations. For vehicles with an OMV of $20,000 or less, you are limited to a 70% loan. If the OMV exceeds $20,000, the maximum loan is 60%. This means you must prepare a down payment of at least 30% to 40% in cash or through a trade in value.

How long must I be a PR before I can apply for a car loan?

You can apply for a car loan immediately after receiving your PR status. While there's no legal waiting period, most banks prefer to see at least 3 to 6 months of stable CPF contributions. If you have a shorter history, providing a letter of appointment or your previous Employment Pass income tax records can help secure a car loan for new permanent resident sg approval.

Is the interest rate different for PRs compared to Singapore Citizens?

Interest rates are generally the same for PRs and Singapore Citizens. Most financial institutions offer rates between 2.48% and 2.78% for new vehicles as of May 2026. Your residency status doesn't change the base rate, but your local credit score and length of employment will determine whether you qualify for the lowest advertised figures. Banks value stability over citizenship status for these assessments.

What happens to my car loan if I leave Singapore before it is paid off?

You must fully repay the outstanding loan balance before you can sell the car or cancel the registration to leave the country. Since the car serves as collateral, the bank holds the title until the debt is cleared. If you plan to move, it's best to settle the loan at least 30 days before your departure to ensure all paperwork is processed by the LTA.

Can I use my CPF to pay for a car loan instalment?

No, you cannot use your CPF savings to pay for car loan instalments. CPF funds are restricted to housing, healthcare, and retirement purposes. Car loan repayments must be made using cash, usually via a monthly GIRO deduction from your personal bank account. It's important to factor this into your monthly cash flow alongside your other residency financial obligations like income tax.

Does a new PR need a guarantor for a car loan?

A guarantor is typically not required for a new PR if you meet the minimum income and TDSR requirements. However, a bank might request one if your local credit history is less than 12 months old or if your debt to income ratio is near the 55% limit. Having a guarantor who is a Singapore Citizen can sometimes help in securing a car loan for new permanent resident sg applications.

What is the minimum income required for a car loan in 2026?

The minimum monthly income required for a car loan in 2026 is $2,000. This is the baseline for most major banks like DBS and OCBC. Keep in mind that while $2,000 is the minimum for eligibility, your actual loan amount is governed by the Total Debt Servicing Ratio (TDSR). This policy limits your total debt repayments to 55% of your gross monthly income.

Can I get a car loan for a parallel import car as a new PR?

Yes, you can definitely get a car loan for a parallel import vehicle. Banks and in-house lenders treat parallel imports the same as those from authorized dealers, provided the car is new or meets the age requirements for used car financing. The same OMV based loan to value limits of 60% or 70% will apply to these vehicles, and the process remains straightforward for PR holders.

In Same Category

- How to Prepare Your Car for Sale in Singapore: The Ultimate 2026 Checklist

- When to Sell Your Car in Singapore: The Strategic 2026 Guide to Maximizing Returns

- Car Dealership Financing vs Bank Loan in Singapore: The 2026 Comparison Guide

- Used Car Warranty in Singapore: The Ultimate Guide to Protection in 2026

- Used Car Service History Check Singapore: The 2026 Ultimate Buyer’s Guide